Convinced and Uncertain at the Same Time

Bitcoin dropped to $58,000 this week—a new bear market low. The cause? Financial market uncertainty as AI trade doubts mount, the dollar rallies, and the Fed's hawkish stance rattles investors.

The hypothesis of recursive self-improvement (RSI) is that AI improves itself, which in turn makes it even better at improving itself. The time between two improvements keeps shrinking, and the leaps keep getting bigger.

We're seeing some evidence of this on a small scale. Apps like ChatGPT and Codex are improving faster and faster as AI within OpenAI takes over more and more tasks from humans. We also see that the doubling time of certain metrics is getting shorter, such as the maximum task length that AI systems can reliably execute (METR).

Optimists extrapolate this trajectory and expect major breakthroughs across practically every facet of life. From superintelligent and highly helpful assistants to autonomous humanoid robots that do all the work humans don't feel like doing. Abundance for everyone.

Pessimists see all kinds of ways this could go wrong, such as mass unemployment, extreme inequality, repressive surveillance, and autonomous warfare. They advocate for a globally coordinated slowdown of AI development and restrictions on its use.

What the optimists and pessimists have in common is the belief that AI will actually disrupt the world in many ways before long. They represent the utopian and dystopian sides of the same coin.

And precisely because this scenario is plausible—the probability is far from negligibly small—everyone feels a sense of urgency.

Countries don't want to fall behind and are investing billions in the five layers of the AI stack: energy, chips, infrastructure, models, and apps. Being at the forefront is a matter of geo-economic and geopolitical importance.

Companies feel their competitors breathing down their necks. If AI truly supercharges productivity, it's existentially important to get on board in time.

Investors are excited and nervous at the same time. Own the winners, and you'll get rich. But which companies are those? And which companies will see AI eat into their profitability?

This collective determination drives impressive market rallies. Dips are bought up at lightning speed, and IPOs are oversubscribed. As The Kobeissi Letter wrote: "Investors know AI is the next big thing, and no one wants to miss the next big thing."

"But, uncertainty is a major byproduct of innovation," the X account continued. And that's primarily what we saw over the past two weeks.

We're witnessing a rare, large-scale technological revolution. The digital world is changing before our eyes. AI analyzes, organizes, writes, produces, and builds. And the physical world is also on the cusp of major transformation, with autonomous vehicles, drones, and humanoid robots.

Bart, Bert, and Peter cover all of this in the new podcast Turing Station. A broad look at the technology, practical applications, and implications for society, the economy, and your investment portfolio. A great complement to Alpha Markets!

Watch & listen on Spotify or YouTube. Or use this RSS feed in your favorite podcast app.

The market expects the war in Iran to be over. Tanker traffic is slowly resuming, and the oil price has fallen to $69, back to pre-war levels. That's a relief, but without the distracting effect of daily threats of war escalation, attention has suddenly shifted to how strong the AI trade really is.

And there are doubts. We'll highlight four.

- The US government is delaying and restricting the rollout of new models like Fable 5 and GPT-5.6. We already knew about Fable, but yesterday it emerged that OpenAI's latest model also needs White House approval. For investors, slower growth and a loss of lead over China is bad news.

- Apple is raising its prices because components like memory have become more expensive. Apple stock dropped 6%. But a bigger consequence is that pricier goods will eventually feed back into inflation. And this is inflation that sticks, even once the Strait of Hormuz reopens.

- The first round of the AI boom is largely behind us. The winners were the suppliers of chips and infrastructure—their stock prices soared. But expectations for future growth are no longer accelerating as fast. The friction of the physical world is becoming visible. Hesitation and doubt are creeping in: Who will be the beneficiaries of the next round? Where should capital rotate to?

- The delay of new models, the stagnation of typical AI stocks, and the steep price drops at SpaceX gave OpenAI reason to leak to the New York Times that they're considering postponing their IPO to 2027.

From the article:

But a cascade of recent developments has caused OpenAI's executives to shift away from their most aggressive aspirations. Top of mind is what has happened to Elon Musk's SpaceX after its I.P.O. this month. [..] Since [the IPO], SpaceX's stock has been on a downward slide.

Global markets have also been choppy in recent weeks, with tech stocks dragging down indexes as investors question whether A.I. companies will live up to their sky-high promises.

The big question is whether the market can once again shake off this doubt, or whether a deeper correction and consolidation is needed. First let some air out of the bubble until the worst overvaluation is gone, or straight to new highs?

What just happened?

— The Kobeissi Letter (@KobeissiLetter) June 25, 2026

In just 27 minutes, the Nasdaq 100 just fell -1,000 points and the S&P 500 erased -$1 TRILLION without any major headlines.

The Nasdaq opened +1% higher then fell -3% between 9:30 AM and 9:57 AM ET.

What does it all mean? Let us explain.

(a thread) pic.twitter.com/HGg3yFeFxz

During the sharply rising and falling phases of a market cycle, markets are driven by internal forces. Enthusiasm on the way up and panic on the way down, accompanied by grand narratives.

Around tops and bottoms, we often see a period of drift. Doubt creeps in about the prevailing narrative, and external forces take over. That's what we're seeing now with bitcoin.

On Wednesday, the price dipped once again to $59,000, the endpoint of the June 5 capitulation. Yesterday, after the Apple panic, the price dropped further to $58,000—the lowest point of this bear market.

This fits perfectly within our base case scenario: the mild bear market. In this scenario, we expect a bottom somewhere this summer, within the $48,000 to $60,000 price range.

Only a weekly close above the 50-week moving average would shift our base case to the bear market being behind us and a new bull market having begun. That dominant moving average has now declined to $89,700.

Until then, we're in a bear market. We've likely arrived at the phase where bottoms are formed. We're transitioning from pessimism and panic to despondency and indifference.

The next step would be catching occasional glimpses of hope. Hope that the bear market will eventually end, that it's not a lost cause, and that bitcoin isn't headed toward irrelevance after all.

We're not seeing that yet—at least not in the places where it matters. Permabulls being bullish is just noise. Hope emerges from positive signals coming from unexpected corners. Like the interest in bitcoin during the US regional banking crisis in March 2023, and BlackRock's application for a bitcoin ETF in June 2023.

So we need to hang in there a bit longer. In the $50,000 to $70,000 zone, we're seeing clear signs of accumulation, with existing investors adding to their positions. That makes sense. If you exited at "the handbrake" between $95,000 and $100,000, these are logical price levels to start rebuilding exposure.

We continue with the following topics for our Alpha Plus members:

- Bitcoin investors are buying the dip

- MSTR and STRC hammered

- Gold, silver, and the dollar

- Micron's quarterly results: an argument against rate hikes?

- Did we reach 'peak hawkishness' from the Fed on Monday?

1️⃣ Bitcoin investors are buying the dip

Bert

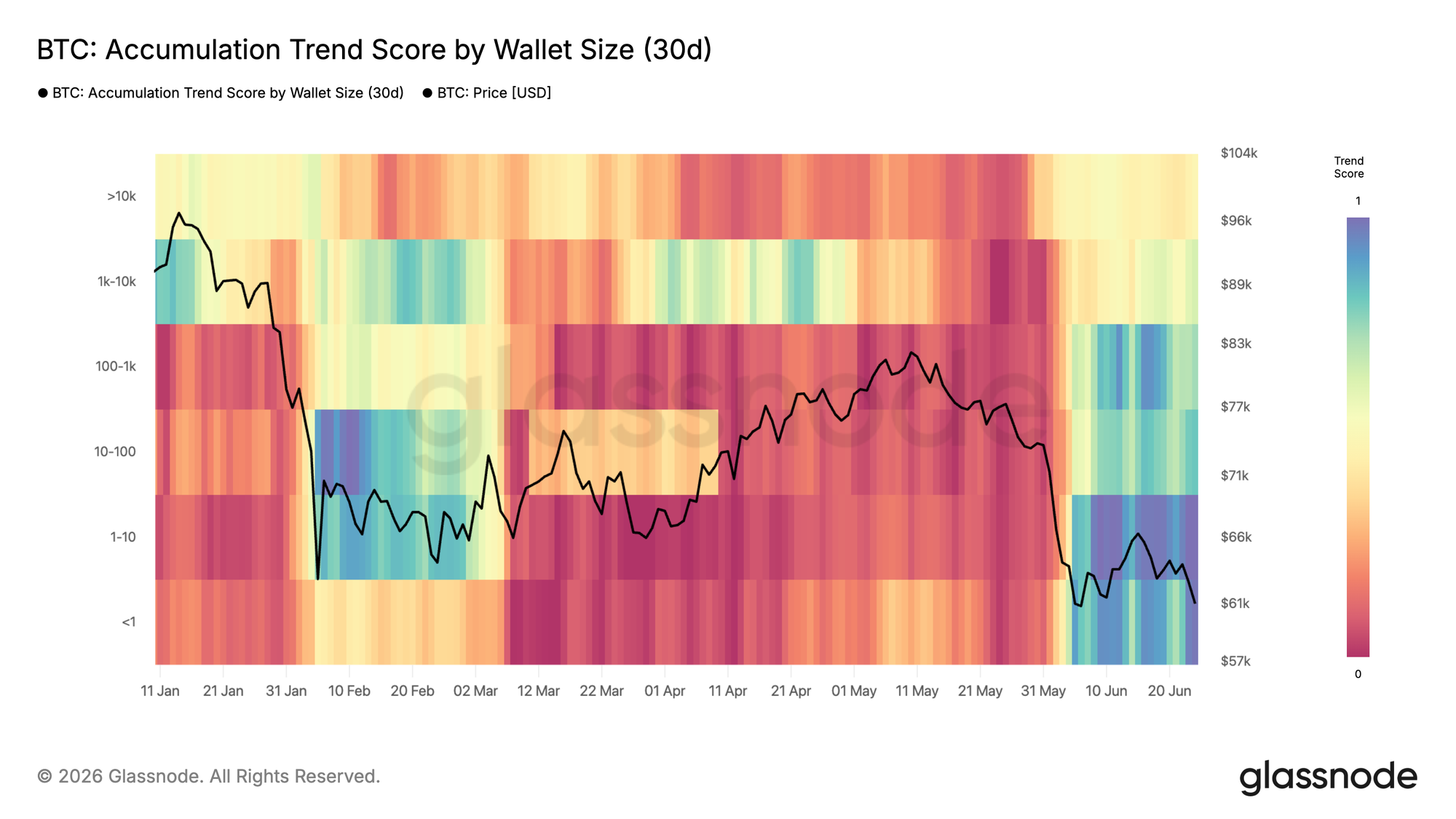

On June 15, Glassnode posted this on X:

The recent BTC correction appears to have attracted buyers back into the market. Accumulation Trend Scores have turned higher across multiple wallet cohorts, suggesting supply is being absorbed as investors step in following the move to down $60K.

This is the chart they included, updated with data through today.

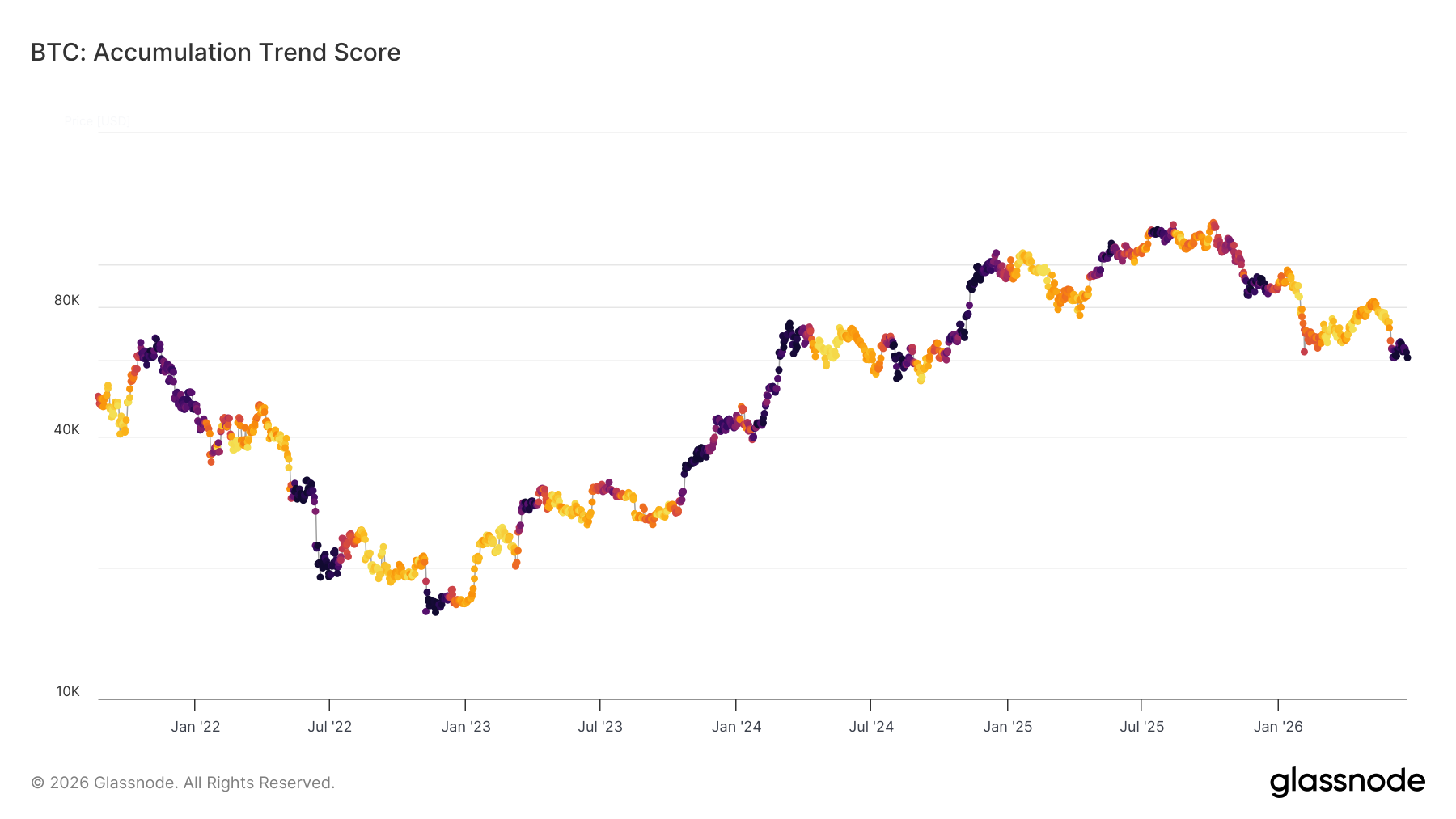

You can also aggregate the accumulation and distribution behavior of the six investor cohorts into a single number between 0 (light yellow) and 1 (black), as shown in the chart below.

In bull markets, we see accumulation during the sharp bullish rallies. In bear markets, it happens after significant capitulation events. That's no guarantee a bottom is forming, but it does show that existing investors have conviction and are buying the dip.

What stands out is that this conviction was absent after the February 6 capitulation—the dots stayed orange and quickly turned yellow again: distribution. After the June 5 capitulation, we immediately see dark data points: accumulation.

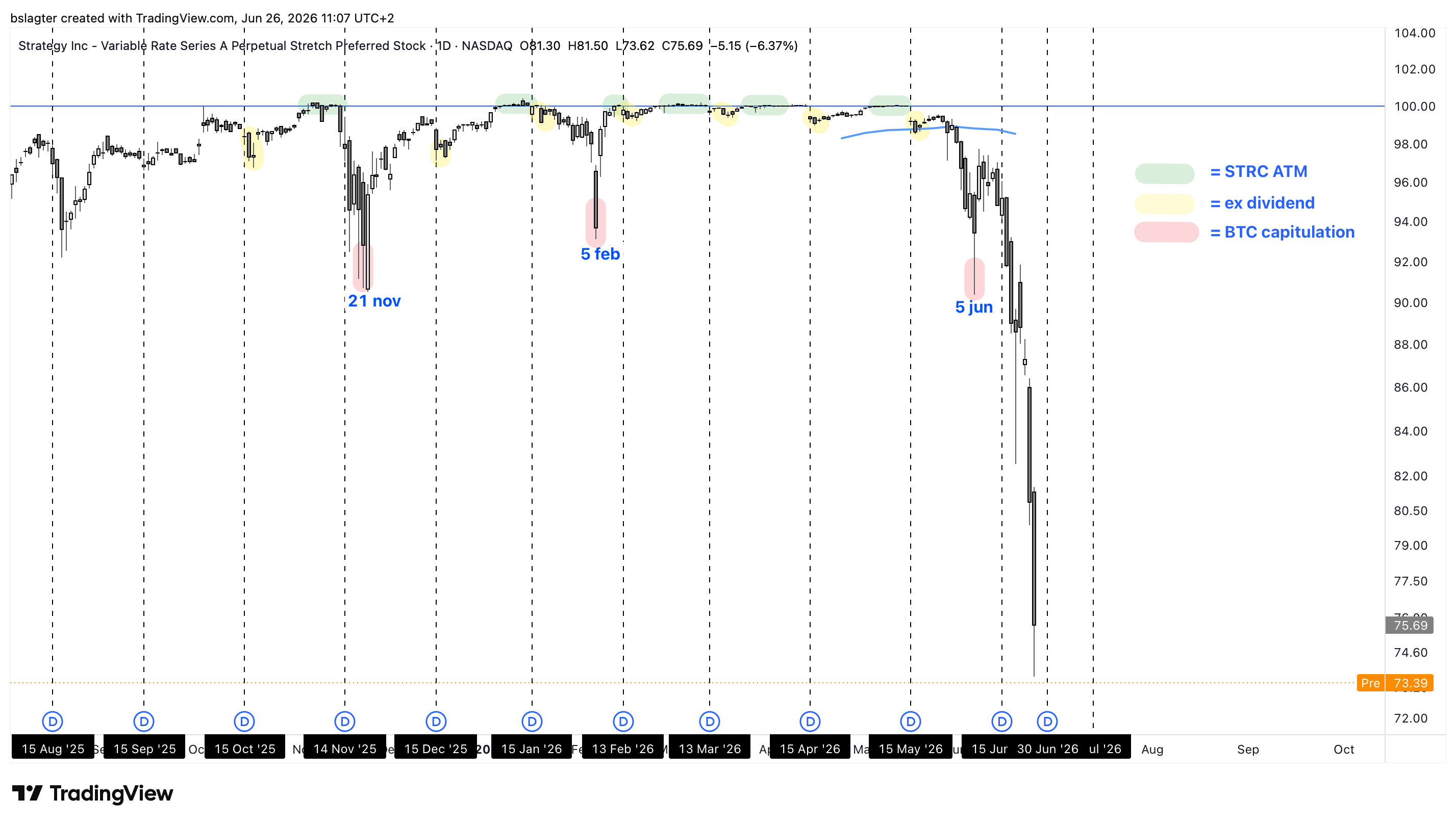

2️⃣ MSTR and STRC hammered

Bert

These haven't been Michael Saylor's best weeks. In early June, bitcoin's price dropped 20% in less than a week from $73,000 to $59,000—the third major capitulation of this bear market. Saylor was singled out as the scapegoat.

For a moment, it looked like the storm would blow over. But that turned out to be a head fake. After June 15, bitcoin's price fell 13% from $67,000 to $58,000. Over the same period, MSTR's stock price dropped nearly 40%.

MSTR is now down over 80% from its peak, and the premium the stock carried above the value of the bitcoin in its treasury has completely evaporated. Investors want nothing to do with the company anymore.

More problematic is the situation with STRC, the preferred stock with characteristics of a perpetual bond carrying an 11.5% yield. Saylor spent months touting it as a safe product, with phrases like "a bank account in cyberspace."

The post on X below illustrates this nicely. A woman sips a drink on a tropical island. She's not on vacation—she lives there. The interviewer asks how she pulled it off. The answer: "I worked hard [..] to save money, then I put my savings into STRC."

For investors who are firmly convinced that bitcoin will appreciate by an average of 30% per year over the next 10 years, it's not a bad product. But marketing it as "similar to a money market fund" is problematic. Setting aside the question of whether it's even legally defensible, it creates the false expectation that STRC's price should always stay at $100.

It's perfectly normal for the price of a preferred stock to fluctuate. Its expected volatility is lower than that of BTC or MSTR, as is the expected return. But it's not zero.

And that's where investors are now paying the price. First, the investors who had bought STRC with heavy leverage, expecting the price would never stray far below $100. They were forced to sell on a massive scale. But also the retail investors who thought they were putting their savings in a Strategy bank account at 11.5% interest.

At the moment, STRC is trading around $75. Hanging over the market is the uncertainty about Strategy's response. Will they raise the dividend? Will they buy back STRC themselves? Will they suspend the dividend? Will they increase their dollar reserves by selling bitcoin? Who knows what Monday will pull out of the hat.

And so Michael Saylor has fallen into the pit he dug himself, by insufferably promising retail investors something that doesn't exist: return without risk.

There were signs pic.twitter.com/2Hg57ZIQxP

— Tom Dunleavy (@dunleavy89) June 25, 2026

3️⃣ Gold, silver, and the dollar

Sam

In the April 3 edition of Alpha Markets, titled Warning Signals from Other Markets, we discussed a potential upside breakout of the dollar index (DXY) and how that could put pressure on risk assets. Last week's close was outside the yellow price range, and this upward trend has continued this week as well.

At the same time, we're seeing weakness in US equities and in precious metals like gold and silver. Silver had dropped more than 20% in just one week since its local top on June 17, and gold was down about 10%.

While those may be "rookie numbers" for anyone who's been active in crypto for a while, for these traditional investments, that's an exceptionally steep decline. And although correlations rarely track perfectly, the correlation between a strong dollar and weakness in precious metals—and vice versa—has been very strong this year as well.

For instance, the dollar fell about 4% from mid to late January, back to the bottom of the yellow price range in the chart above. Then the dollar rallied all the way back to the top of the yellow range in February and March.

During January's dollar decline, silver surged 70% and gold 30%. Between the late January peak and the end of March, when the dollar showed strength, silver dropped 50% and gold fell 27%.

If we assume this correlation persists, it's wise to wait before buying precious metals until this dollar rally comes to an end.

Of course, we don't know when that will happen, but 106 in particular—the top of the white price range—has served as strong support and resistance on multiple occasions. If the price doesn't reach that level, the formation of a lower low on the daily chart is something to watch for.

However, the single most important signal would come if the DXY falls back into the yellow price range below 100. This will most likely coincide with precious metals that have already bottomed, but it would serve as additional confirmation.

For silver, a logical area to bottom would be between $48 and $54. For gold, that corresponds to a bottom somewhere between $3,200 and $3,500.

These figures are based on the assumption that the DXY doesn't break out above the white price range or fall back into the yellow range in the near term. If either of those things happens, these plans change. In other words: strong opinions, loosely held.

4️⃣ Micron's quarterly results: an argument against rate hikes?

Thom

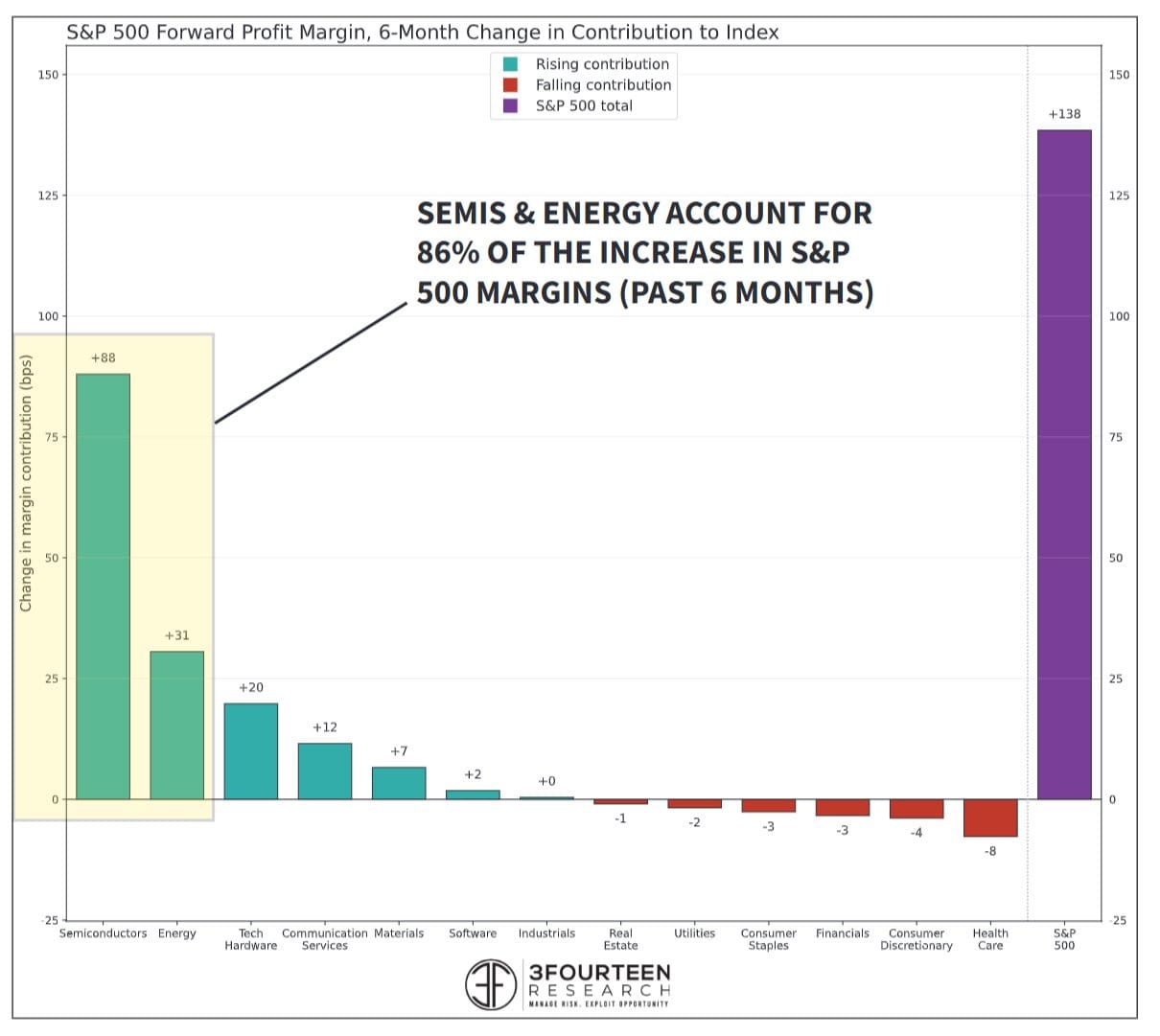

While the S&P 500 has risen sharply in recent years, valuations have remained reasonable because earnings have grown nearly as fast. Micron's (MU) strong numbers from last Wednesday were no exception. There were serious doubts beforehand, but Micron convincingly breathed new life into the AI rally.

For now, the strong stock market gains continue to be supported by equally impressive growth in earnings and margins.

The risk lies primarily in the composition of that earnings growth. It leans heavily on chip companies and the energy sector. Together, they accounted for 86 percent of the increase in profit margins within the S&P 500 over the past six months.

This is an argument against rate hikes. A large part of the economy is not overheating at all. Growth is primarily driven by the wealthier consumer and the AI sector. These parts of the economy are relatively insensitive to higher interest rates.

The ones that rate hikes actually hurt are the businesses and consumers already struggling with higher borrowing costs.

That's why it seems highly unlikely to me that the Fed would actually proceed with rate hikes at this point. Especially now that the oil price has fallen back below pre-war levels, economic momentum is finally picking up slightly, and PMIs are tentatively beginning to recover.

It also seems highly unlikely to me that the Fed would hike rates heading into the midterm elections in November 2026. Also because the economy relies so heavily on the AI sector that a correction there alone would be enough to fully eliminate inflation concerns.

5️⃣ Did we reach 'peak hawkishness' from the Fed on Monday?

Thom

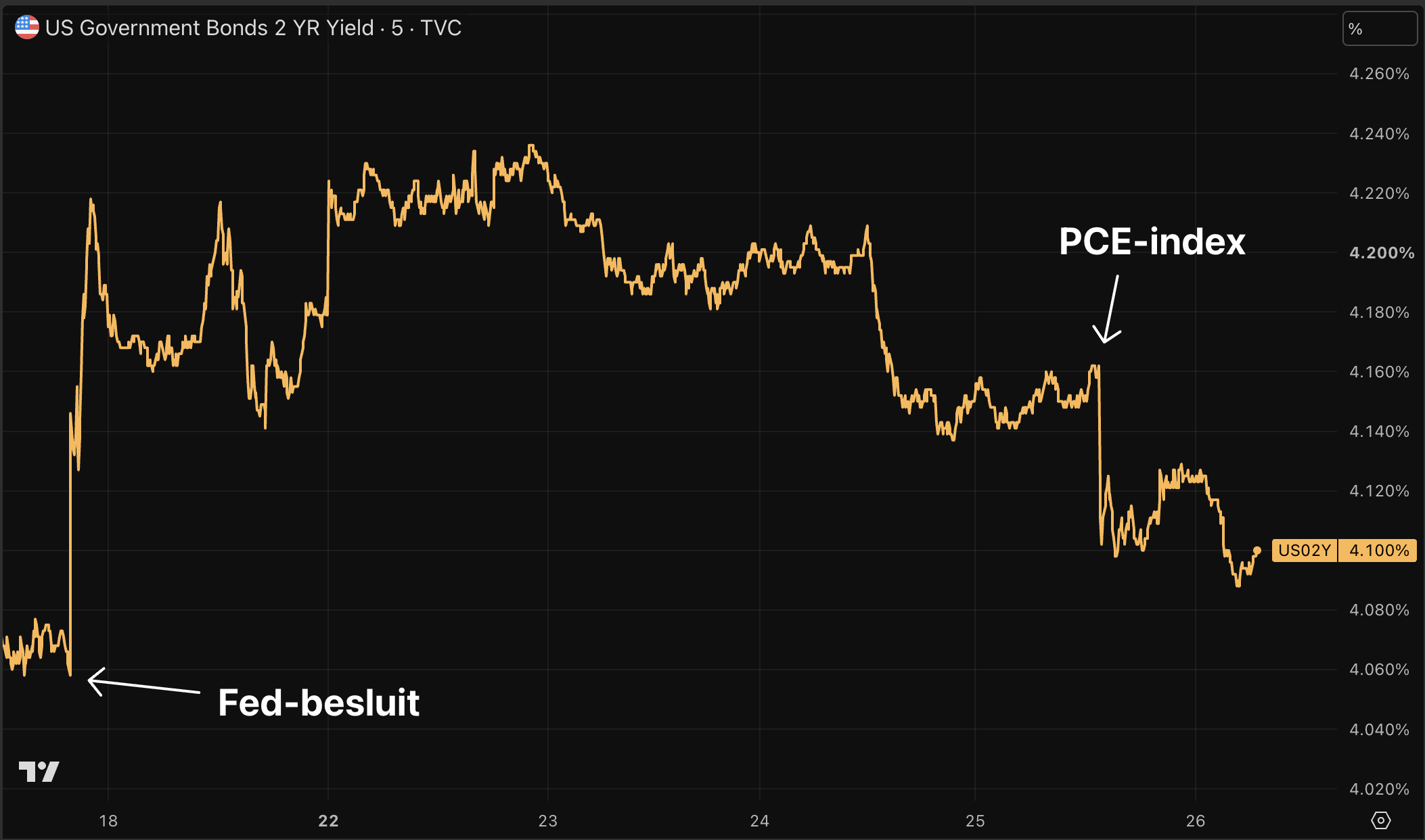

After last Wednesday's Fed rate decision, which the market interpreted as hawkish, bond yields jumped. Rate hikes are suddenly back on the table, despite the oil price falling back to pre-Iran war levels.

This suggests that both the Fed and the market believe the inflation problem runs deeper than the energy market alone.

That gave yesterday's PCE inflation print the potential to deal a serious blow to bitcoin and the rest of the financial markets. If the core PCE index—which strips out energy—came in hotter than expected, it would have confirmed the market's fears.

In the end, the monthly increase for core PCE came in at 0.32 percent. That was on the low end of expectations, but still the fourth-highest monthly increase of the past twelve months. On an annualized basis, that works out to 3.9 percent.

The twelve-month increase stands at 3.4 percent—the highest since October 2023. The annualized increase over the past six months is above 4 percent.

Yet the market doesn't seem too worried about this for now. After the rate decision, the 2-year yield shot up sharply, but much of that increase has already been given back. After yesterday's PCE print, yields fell further still.

This cautiously paints the picture that Monday was the moment of 'peak hawkishness'—the point at which the market began pricing in the most aggressive version of the rate path.

Today, four days later, the market is still pricing in one and a half rate hikes in 2026. A full return to the no-hike scenario is therefore not on the cards yet.

What we're mainly seeing now is a shift from the most hawkish rate path to a slightly less hawkish scenario. That gives assets like bitcoin and gold some breathing room. At the same time, it means there's theoretically even more room for recovery if the market ultimately prices out rate hikes entirely.

That seems to me the most likely scenario in the end. There are plenty of reasons to believe inflation will cool in the coming months. The effect of Trump's tariffs is starting to fade, and a solution for the Strait of Hormuz appears to be in the works.

On top of that, housing inflation will likely continue to cool in the months ahead, and the labor market is not currently generating any clear additional inflationary pressure.

The vulnerability of AI stocks also plays a role here. A 10 to 20 percent correction in that corner of the market could be enough to push inflation concerns into the background. After all, the US economy currently leans heavily on the investment wave surrounding artificial intelligence.

All things considered, I believe there are sufficient reasons to be cautious about new rate hikes—or at least to hold off for now. That's why my base case remains that the Fed will ultimately not raise rates in 2026.

In closing

All previous editions of Alpha Markets can be found in the archive. Questions, comments, and suggestions are always welcome in the community.

Thank you for reading!

To stay informed about the latest market developments and insights, follow our team members on X:

- Bart Mol (@Bart_Mol)

- Peter Slagter (@pesla)

- Bert Slagter (@bslagter)

- Mike Lelieveld (@mlelieveld)

We appreciate your continued support and look forward to bringing you more comprehensive analysis in our next edition.

Until then!