Bigger Than Saylor?

The Hunt Brothers once cornered the silver market. What does their story tell us about Michael Saylor, Strategy, and the recent turmoil around bitcoin?

Peter

You can hardly have missed that the bitcoin price dropped below $60,000 last week. Michael Saylor has been cast as the scapegoat, having sowed doubt about the long-term viability of his company with a series of balance sheet decisions. "[The bitcoin price dropped] after American entrepreneur, billionaire, and above all bitcoin guru Michael Saylor himself sold bitcoin to pay his investors," NU.nl explained to its readers.

For years, Saylor was the man who never sold. He bought, borrowed, raised capital, and bought again. His company became a publicly traded leveraged bet on bitcoin, with a CEO who spoke as if selling were a character flaw. The moment someone like that lets go of even a few coins, the market starts thinking. Especially when he'd just narrowed the crumple zone around his leverage. What if the largest corporate buyer ever has to pull the emergency brake?

Selling 32 Bitcoin proved several important things:

— Fred Krueger (@dotkrueger) June 2, 2026

✅ Posting "Buying Bonds" was a bad idea

✅ Selling any amount of BTC was a bad idea

✅ Cutting to 6mo of dividend coverage was a bad idea

✅ Posting ads on how STRC held its peg was a bad idea

✅ Odds of SP500 inclusion: 0%

That question is less novel than you might expect. Back in the 1970s, the silver market was watching two brothers from Texas in much the same way.

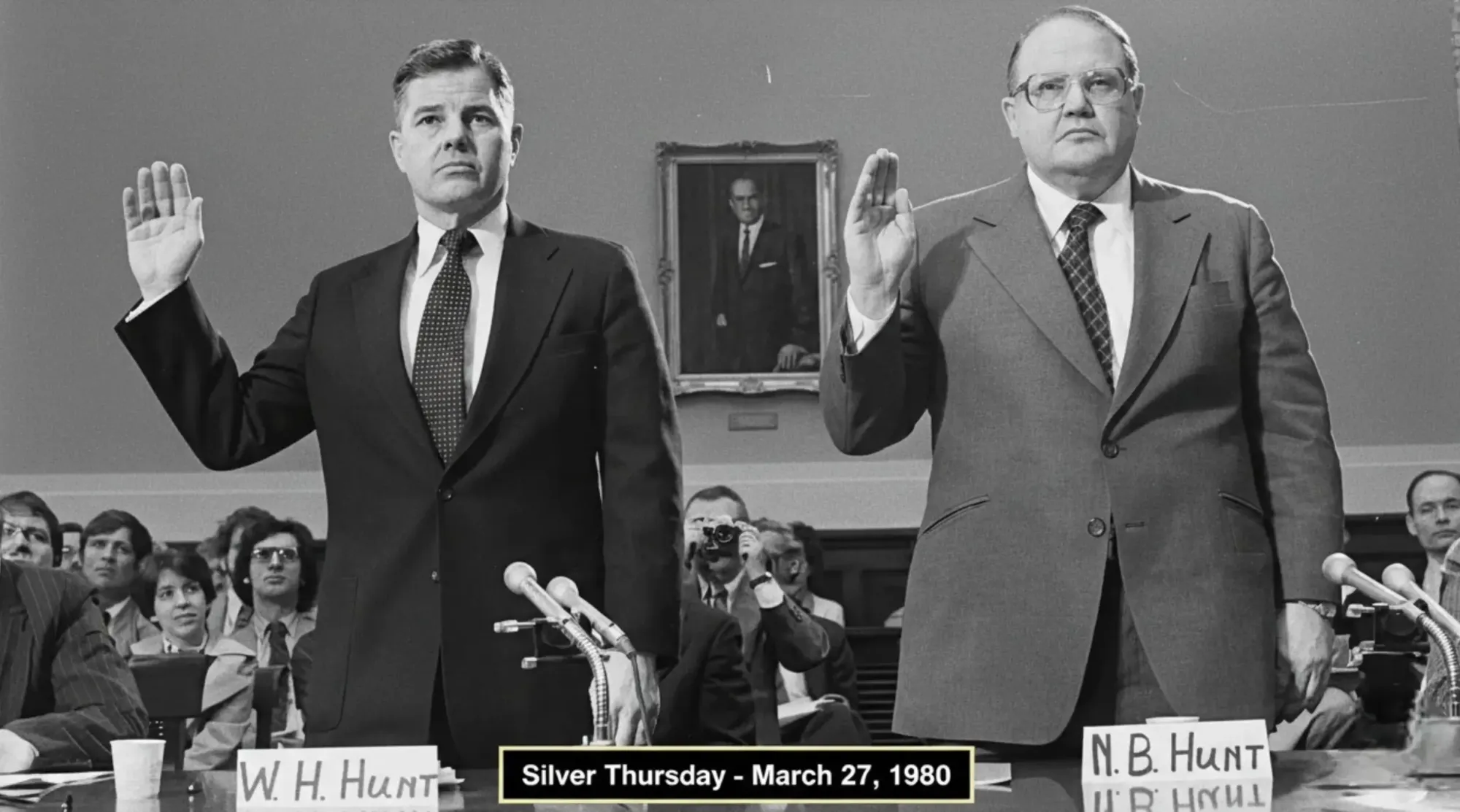

Texas stood for oil, land, horses, big houses, and even bigger egos. The Hunt family fit right in. Father Haroldson was born in 1889, grew up on a farm in Illinois, and worked his way—without any formal education—into becoming one of America's greatest oil tycoons. On the day he died, he left one of the largest fortunes in the world to his family.

Hunt had fifteen children by three women. One son, Lamar, founded the American Football League and came up with the Super Bowl. Two other sons, Nelson and William, would become the protagonists of a different kind of legend.

These brothers grew up in a world of wealth, stubbornness, and distrust. The 1970s fed that distrust generously. Nixon had severed the last link between the dollar and gold in 1971. Then came oil crises, high inflation, and a dollar that felt increasingly shaky. The Hunts saw a monetary system that had lost its anchor.

The brothers wanted to hedge against the doomsday scenarios that come with an unmoored dollar. They did so with a reflex that many bitcoiners will recognize: buy something that can't be printed.

You might think of gold first. But that was tricky for Americans. Private ownership of gold bars had been severely restricted since the 1930s and wasn't legalized again until late 1974. Silver was the more obvious choice. It was freely tradable, cheaper, and, according to the Hunts, massively undervalued. And so… they opened their wallets.

It started with small, local purchases. But as the appetite for silver grew, the brothers entered the global market. They bought futures contracts and, unlike common practice, actually took physical delivery of the underlying silver. They wanted to hold the real thing. The metal disappeared from the market and showed up in vaults in Switzerland, London, and the US. It became a massive logistical operation.

By late 1979, they held hundreds of millions of ounces. It's often said they directly or indirectly controlled roughly a third of the freely tradable silver supply. Naturally, that showed in the silver price. It surged more than 800 percent in a single year, from $6 to $50 per ounce. Jewelers and manufacturers watched their raw material become nearly unaffordable in a matter of months. Tiffany & Co. even took out an ad in The New York Times to publicly attack the brothers. A couple of billionaires, the company argued, were draining an essential commodity from the market.

The Hunts saw it differently. In their view, they were simply protecting their wealth against an inflationary enemy: paper money. But as the silver market fell increasingly under their influence, the critics grew louder. They spoke of an attempt to corner the silver market. Somewhere along the way, the Hunts' position grew so large that their intentions mattered less than the consequences.

That's where the first crack appeared in the brothers' silver empire. The rise in the silver price had become so extreme that regulators and exchanges grew nervous. They made it harder to maintain enormous silver positions with borrowed money. For the Hunts, the timing couldn't have been worse. They had financed a large part of their strategy with credit. When the price started falling, banks and brokers demanded additional collateral. Money the brothers didn't have readily available. On March 27, 1980, they couldn't meet a margin call of roughly $100 million. The panic that followed went down in history as Silver Thursday.

Ultimately, a $1.1 billion credit line was needed to prevent the market from being held hostage by the Hunts' obligations. But the damage was already done. The silver price had collapsed and their fortune evaporated. Lawsuits, fines, trading bans, and bankruptcy proceedings followed. The men who rode silver to the moon became a cautionary tale about leverage, tunnel vision, and market power.

Michael Saylor could have been one of the Hunt Brothers. It's not a perfect analogy—compared to the grip the Hunts had on silver, Saylor still has a long way to go. The similarity lies in how the market perceives it. A scarce asset can temporarily become so closely tied to a single buyer that everyone starts staring at him. For silver, that was the Hunts. For bitcoin, it's Saylor. That's why the sale of 32 BTC felt bigger than it was, and why the balance sheet of one company is momentarily draped over an entire monetary system.

Maybe the accompanying doubt will blow over quietly. Maybe Strategy will prove more vulnerable than many bitcoiners want to admit. For bitcoin, that's the question of the week. Has digital gold become a Saylor story, or is bitcoin bigger than Saylor?

For the answer, we can look back at the Hunts. There was a moment when investors wondered whether the silver price could still be seen separately from two brothers in Texas. In the end, the question turned out to be more important than the answer. Because when the brothers disappeared, silver simply carried on.

More Alpha

Are you a Plus member? Then we continue with the following topics:

- Claude finds vulnerability in Zcash

- First Fannie Mae mortgage with bitcoin as collateral

- The coldest winter is all in your head

Below that, you'll find the news snacks—a handy overview of the news that actually mattered last week.

1️⃣ Claude finds vulnerability in Zcash

Erik

Last Thursday, Zcash founder Zooko Wilcox posted a message on X about a dangerous vulnerability in the protocol. The bug, discovered by a researcher commissioned by Zcash itself, had been patched. All's well that ends well? Not quite. What's thought-provoking is that the bug was found with the help of a publicly available AI model, Claude Opus 4.8. What does this mean for the near future of DeFi hacks?

The bug was in Orchard, a pool for Zcash users who opt for the built-in privacy feature. Orchard launched in 2022. Zcash also maintains its older pools, which run on legacy technology, for users who don't want to move their coins.

The bug could have allowed an attacker to illicitly obtain ZEC. What caused considerable alarm was that it couldn't be ruled out whether the bug had already been exploited by an attacker before the white hat discovered it. According to Wilcox, however, this is unlikely.

No infinite inflation

An important nuance that gets lost in some reporting: the vulnerability could not have led to infinite inflation of the Zcash supply, as Decrypt explained. The hacker could only have stolen from other Zcash holders in the Orchard pool. Zcash has a "turnstile" that ensures no more can ever flow out of a pool than provably went in. So the total ZEC supply couldn't have been inflated. However, the pool could have become insolvent.

The way to understand the ZCash bug is it's not infinite mint of ZEC itself. It's more like the shielded pool (Orchard) could become insolvent. Think of it more like the KelpDAO hack for ETH.

— Doug Colkitt (@0xdoug) June 5, 2026

Very little reason not to proactively unshield any ZEC today. Being early to the exit… pic.twitter.com/jMunPMexgS

Privacy as a bug, not a feature

On many networks that enforce privacy, sender and receiver details are hidden behind zero-knowledge proofs. Compare this with bitcoin, where everything is out in the open. In that context, double spends and other irregular transactions are immediately visible. Zcash's privacy pool is specifically designed to conceal transactions. The chain only stores proof that the rules were followed, not what happened. You could say: "What happens in the pool, stays in the pool." Every advantage has its disadvantage, as this case proves once again…

Udi Wertheimer put it as follows:

"The issue isn't that the bug existed. The issue is that zcash, unlike almost any other cryptocurrency, enables a unique class of bugs, where if they're exploited no one would know. This unique class still exists. The fact that they fixed this specific bug is immaterial. Mythos could find 8 others."

The fix

Zcash fixed the problem in stages. On June 2, a soft fork in preparation for the definitive hard fork that followed a day later. The price only crashed when the post-mortem was published on Thursday. ZEC dropped about 38% on the day, and ultimately more than 50%, from a peak around $635 to a low around $310, with over $100 million in liquidations.

Zcash promoter Arthur Hayes closed his entire ZEC position. Not because he thinks the bug was exploited, but because it can't be cryptographically ruled out. The very privacy that makes Orchard valuable makes the supply unauditable.

The implications for the entire DeFi market

As mentioned, the bug was found with the help of Anthropic's Opus 4.8, a publicly available AI model. There's been a lot of discussion in recent months about Mythos, the cutting-edge model that Anthropic won't release to the world due to serious cybersecurity concerns.

Over the past two years, the center of gravity in crypto attacks shifted away from hacks, toward human vulnerabilities. Social engineering dominated the hack landscape in 2025.

It's conceivable that we'll see a resurgence of purely software-based hacks, like in the early days of DeFi around 2020 and 2021. At the very least, an arms race will emerge. Many more protocols will do what Zcash did: deploy AI to protect their networks against AI-accelerated hacks.

Zcash got lucky: this time, the defense found the bug first.

2️⃣ First Fannie Mae mortgage with bitcoin as collateral

Peter

Buying a house without selling your bitcoin. In Michigan, it's been done for the first time within a Fannie Mae-backed mortgage.

Joe and Amy, a couple from Ann Arbor, closed a conventional mortgage through Coinbase and lender Better, using bitcoin as collateral. The bitcoin collateral was used to fund the down payment.

The structure consists of two parts. The first loan is a standard mortgage that falls within Fannie Mae's guidelines. Normally, that loan also covers the down payment, but here it's been split. The second loan component is backed by Joe and Amy's bitcoin holdings. They don't have to sell their bitcoin, avoid taxes on realized gains, and maintain exposure to the bitcoin price.

According to Better, normal price fluctuations won't trigger margin calls or liquidations. The pledged collateral only truly comes into play if the homebuyer persistently and structurally fails to make payments. That should be reassuring for Joe and Amy, because last week bitcoin showed its volatile side. Bitcoin is increasingly taken seriously as a financial building block, but that doesn't mean you can—or should—build everything with it.

The move follows a policy shift at the US mortgage regulator FHFA. Director Bill Pulte ordered that crypto on regulated exchanges be counted toward mortgage applications. Coinbase and Better plan to roll out the product more broadly this summer, initially with support for bitcoin and USDC.

In the Netherlands, this seems less relevant for now. Dutch homebuyers can often finance up to 100% of their property value. Still, the concept could become interesting for people who fall just short of their maximum mortgage and would rather not sell their bitcoin. For now, that option is reserved for wealthy clients of (private) banks that can offer bespoke solutions.

3️⃣ The coldest winter is all in your head

Peter

Joe Weisenthal calls it the coldest crypto winter ever. Not because the bitcoin price is heading to zero, or because the industry is grinding to a halt. But because the party is happening somewhere else.

12 REASONS WHY IT'S THE COLDEST CRYPTO WINTER EVER

— Joe Weisenthal (@TheStalwart) June 2, 2026

Back in February I wrote a list of 10 reasons why this the worst crypto winter ever.

Well everything I cited then still holds, but now I have 2 more ways it's gotten worse:

From the newsletter https://t.co/25c7dc8ulW pic.twitter.com/U1cJTKkHnj

AI stocks are going through the roof. Quantum stocks are soaring at the exact moment bitcoiners are worried about quantum computers. Gold did what bitcoin was supposed to do. Stablecoins have taken over bitcoin's role within the crypto world. And Strategy, the market's great bitcoin vacuum cleaner for years, is now active as a seller.

It's a painful rundown. And yet, every point is debatable.

The institutional adoption cited, for instance, is far from "done." The ETFs have only been around for a short time. Pension funds, sovereign wealth funds, banks, and asset managers are still in the hallway, not the living room. Regulation could shift much further too. And the idea that bitcoin has no role left feels premature. Stablecoins are useful, but they're essentially digital dollars. Bitcoin is something else entirely.

But sentiment doesn't care about facts. And on that front, Weisenthal dissects the market expertly. It feels cold because everyone else is warm. Crypto hasn't just declined—crypto has become boring. And that's worse.

I largely think of "crypto" as a failed asset class at this point.

— Alex Krüger (@krugermacro) June 3, 2026

I've written about the causes multiple times. Mainly, most crypto assets are worthless, or have dreadful value accrual, and most founders have abused the lack of guardrails and dumped on people indiscriminately,…

Finfluencers have since turned this into a new bear market narrative: crypto no longer needs bitcoin. According to them, it's now about real applications, real revenue, and real users. They point to tokens tied to AI projects, privacy, and decentralized exchanges. Those outperformed bitcoin in recent months. And so: after this winter, only tokens that can pay their own way will matter.

Here too, cause and effect are cheerfully mixed up. AI projects are riding the wave because AI is popular. Privacy got big because a few loud voices pushed the narrative hard. Perps platforms caught a tailwind because they were in the right place at the right time—including during the Iran crisis, when traders wanted access to commodity markets outside regular trading hours.

How fleeting such a narrative can be was on full display with Zcash. For a moment, privacy looked like the new normal. Then one bug later, the price dropped, the story took a less rosy turn, and the voices went quiet again.

That's the old crypto lesson in a new disguise: narrative follows price. First the price moves, then the market finds a story to match. Nobody knows what the next bull market's narrative will be; the price has to do its work first.

🍟 Snacks

To wrap up, some quick bites:

- Hong Kong continues building a fully regulated crypto sector. The China-facing metropolis aims to regulate not just trading platforms and stablecoins, but also custodians, asset managers, and advisors under a licensing regime. This creates a supervisory chain covering virtually every link of the industry. Hong Kong wants to further position itself as a financial hub for digital assets, partly by making itself an attractive home base for major players.

- Japan increasingly views stablecoins as a geopolitical tool. The ruling party wants to deploy yen stablecoins for cross-border payments in Asia and is also pushing for a legal framework for crypto ETFs. Behind both proposals lies the same concern: the growing dominance of dollar stablecoins. Globally, governments are increasingly treating stablecoins as infrastructure for international payments. This gives rise to a digital economy with an underlying battle: which currencies will play a central role in it.

- The Philippines pulls the plug on an ambitious blockchain voting project. The measure cuts the proposed budget by approximately 6 billion pesos, equivalent to over $100 million. According to the election commission chair, the technologies are not essential for organizing elections, and concerns about costs and privacy outweigh the benefits. The Philippines spent years exploring how blockchain technology could make elections more transparent and auditable. For now, the calculator wins out over innovation.

- Polymarket is under fire from both regulators and its own users. In South Korea, police are investigating Polymarket users for the first time for illegal gambling. Meanwhile, controversy erupted around a market on whether Strategy would sell bitcoin before May 31. After it turned out the company had indeed sold 32 BTC, Polymarket decided to settle the market as "no," because the information only became public later. The incident touches on a question prediction markets sometimes wrestle with: who ultimately decides what's true?

- Even Charles Hoskinson is worried about Cardano. The founder warns of a new wave of bankruptcies and departing projects, after analytics platform TapTools shut its doors. According to Hoskinson, the ecosystem lacks funding, decisiveness, and governance muscle. The community recently even voted against funding the annual Cardano Summit. The price of ADA dipped below 20 cents, its lowest level in more than five years. On Thursday, Hoskinson announced he was taking a "break." How long he'll be gone is unknown.

- CME Group has launched 24-hour trading for crypto futures and options. The expansion gives investors weekend access to regulated digital asset derivatives for the first time. During the first trading weekend, more than 7,200 contracts changed hands, representing approximately $50 million in notional value. For years, traders looked at Monday's infamous "weekend gap" between CME's Friday close and the bitcoin price on Sunday evening. That era is now over.

- Charles Schwab is working on expanding its crypto services for wealth managers. Starting in 2027, financial advisors will be able to buy, trade, custody, and transfer crypto through the broker. This gives asset managers access to the same infrastructure for bitcoin and ether as retail clients. The move fits a broader trend in which established financial institutions are increasingly looking to offer every part of the crypto value chain themselves.

Thank you for reading!

To stay informed about the latest market developments and insights, follow our team members on X:

- Bart Mol (@Bart_Mol)

- Peter Slagter (@pesla)

- Bert Slagter (@bslagter)

- Mike Lelieveld (@mlelieveld)

We appreciate your continued support and look forward to bringing you more comprehensive analysis in our next edition.

Until then!