A Secular Turning Point

Inflation spikes as the Iran war reshapes markets. Stocks keep setting records while central banks are painted into a corner. Meanwhile, bitcoin grinds through its bear market—caught between a K-shaped economy and AI's insatiable hunger for capital.

Many of the stories that capture our attention have a resolution in the near future. A few months, maybe a few years. Elections, recessions, armed conflicts, the rise of AI, bull and bear markets.

Many are cyclical in nature, remarkably often with a rhythm of around four, five, six years. Driven by a business cycle, commodity cycle, refinancing cycle, liquidity cycle, or election cycle.

While we're busy with all that, much slower movements are unfolding in the background: secular trends. The word secular stems from the Latin saeculum, meaning century or human lifetime.

If you zoom out far enough, surveying the centuries, you'll see that secular trends are also pendulum swings. But with a rhythm so slow that hardly anyone experiences multiple full turns in their lifetime.

The year 2020 is a secular turning point.

For decades, the world leaned on the stability that emerged under American leadership after the end of the Cold War. Trade flourished, countries specialized, and interdependence grew. Production and supply chains spanned the entire globe.

Their fragility became painfully visible in 2020 and the years that followed. Some things, like food, energy, and medicine, are better produced domestically. And it's not exactly convenient that China can remotely shut down your telecom and energy systems. Or that America effectively controls all cloud software.

Zoltan Pozsar, then an analyst at Credit Suisse, predicted in 2022 that countries would shift to a regime of re-arm, re-shore, re-stock, and re-wire. Reinvesting in defense, bringing production back home, maintaining larger stockpiles, and building out energy infrastructure. He called it right.

This deglobalization is expensive and the required investments claim a portion of productive capacity. That leads to higher inflation and rising government debt. And consequently, higher interest rates.

This new regime doesn't affect everyone equally. The consequences differ by individual, company, sector, and region. Think of the K-shaped economy we discussed last week on Satoshi Radio, and wrote about last Monday in the Alpha News.

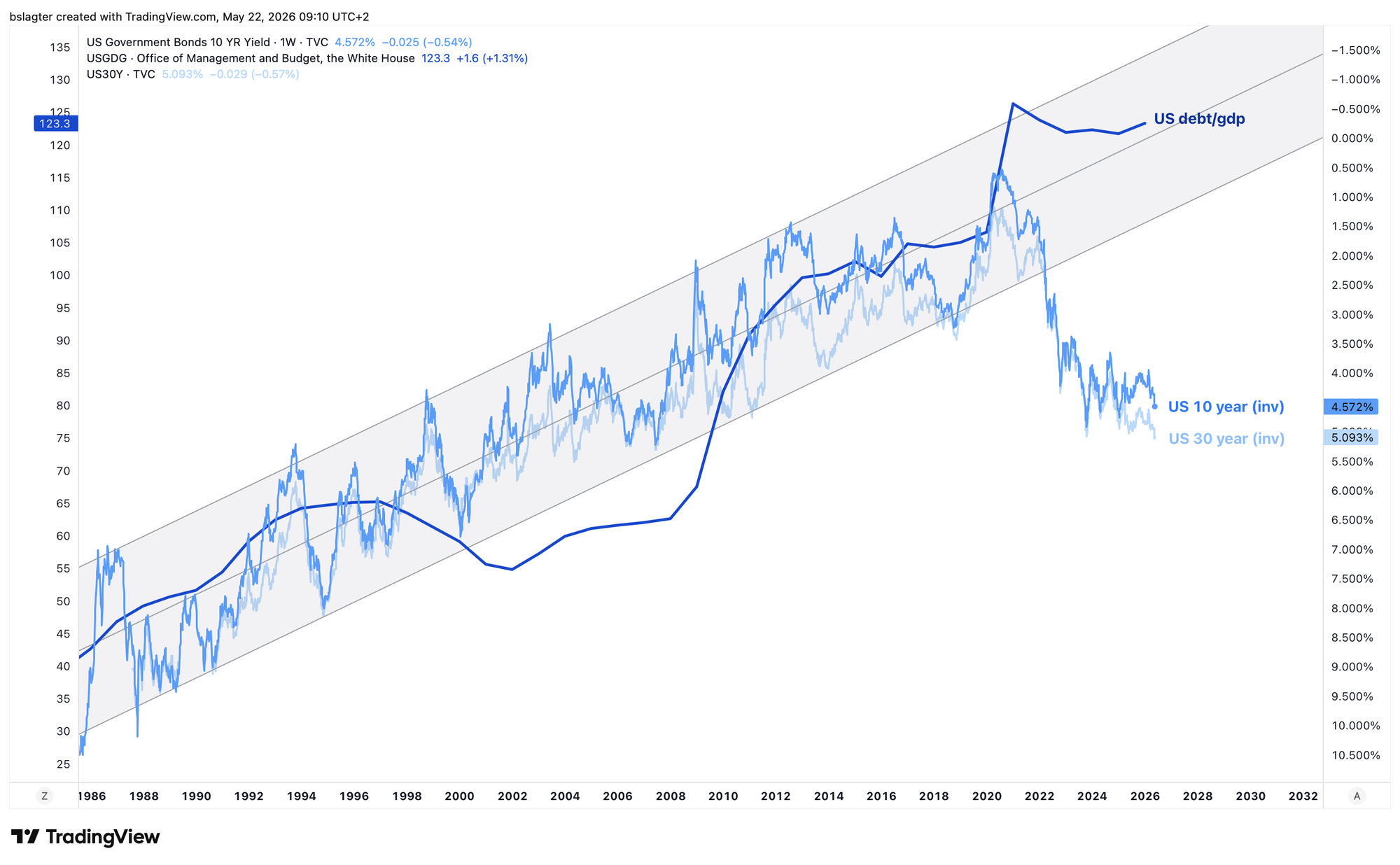

One of the channels through which this inequality spreads is interest rates. The chart below illustrates this. The dark line represents the debt-to-GDP ratio: government debt as a share of the economy.

For 50 years, the debt burden of governments, businesses, and households has been climbing. Only government debt is shown here, but private debt rose more or less in tandem. The direct burden you feel from debt is the amount of interest you have to pay. That amount depends on the principal and the interest rate. After all: 10% on €100,000 equals 1% on €1,000,000.

The lighter lines are the 10- and 30-year yields in the US.

But inverted — look at the right y-axis. The rise in the chart represents the decline in interest rates. This shows that falling rates and rising debt moved in lockstep. In other words, the actual interest burden didn't change all that much. More debt, without really feeling it.

The turning point is 2020. Rates are no longer falling but beginning to rise. While debt keeps climbing relentlessly. And that could start to hurt households, businesses, and governments. Not today, but over the next 10–20 years.

Governments and central banks don't have a whole lot of options to turn the tide. They've painted themselves into a corner, so to speak. Let's walk through the options.

The first option is playing with interest rates. But raising rates to fight inflation causes pain throughout the economy. That pain is unevenly distributed, which leads to social unrest. Lowering rates to keep debt manageable fuels additional demand, which can cause even more inflation.

The second option is boosting economic growth. With debt, it's always about the ratio between debt and earning capacity. For households, it's debt vs. income. For businesses, debt vs. revenue or profit. And for governments, debt vs. the size of the economy.

If the economy grows by 10% and debt grows by 5%, then the relative size of the debt shrinks by 4.5%. The hope now is that AI will deliver a leap in productivity, and thereby drive economic growth.

The room to maneuver is limited. Ideally, governments would keep rates slightly below inflation, so debt slowly melts away. And with a few tailwinds on economic growth, we can kick the can down the road for another decade.

However, a series of inflation shocks keeps throwing a wrench in the works. Caused by the COVID lockdowns in 2020 and 2021. Energy, food, and commodities from Russia and Ukraine in 2022 and 2023. Trump's trade war in 2025. Energy and commodities from the Persian Gulf in 2026.

Ideally, you'd let those high prices do their work. They restore the balance between supply and demand by suppressing demand and rewarding producers for additional supply. But the risk of untreated inflation is that higher inflation becomes entrenched in the economic thinking of households and businesses.

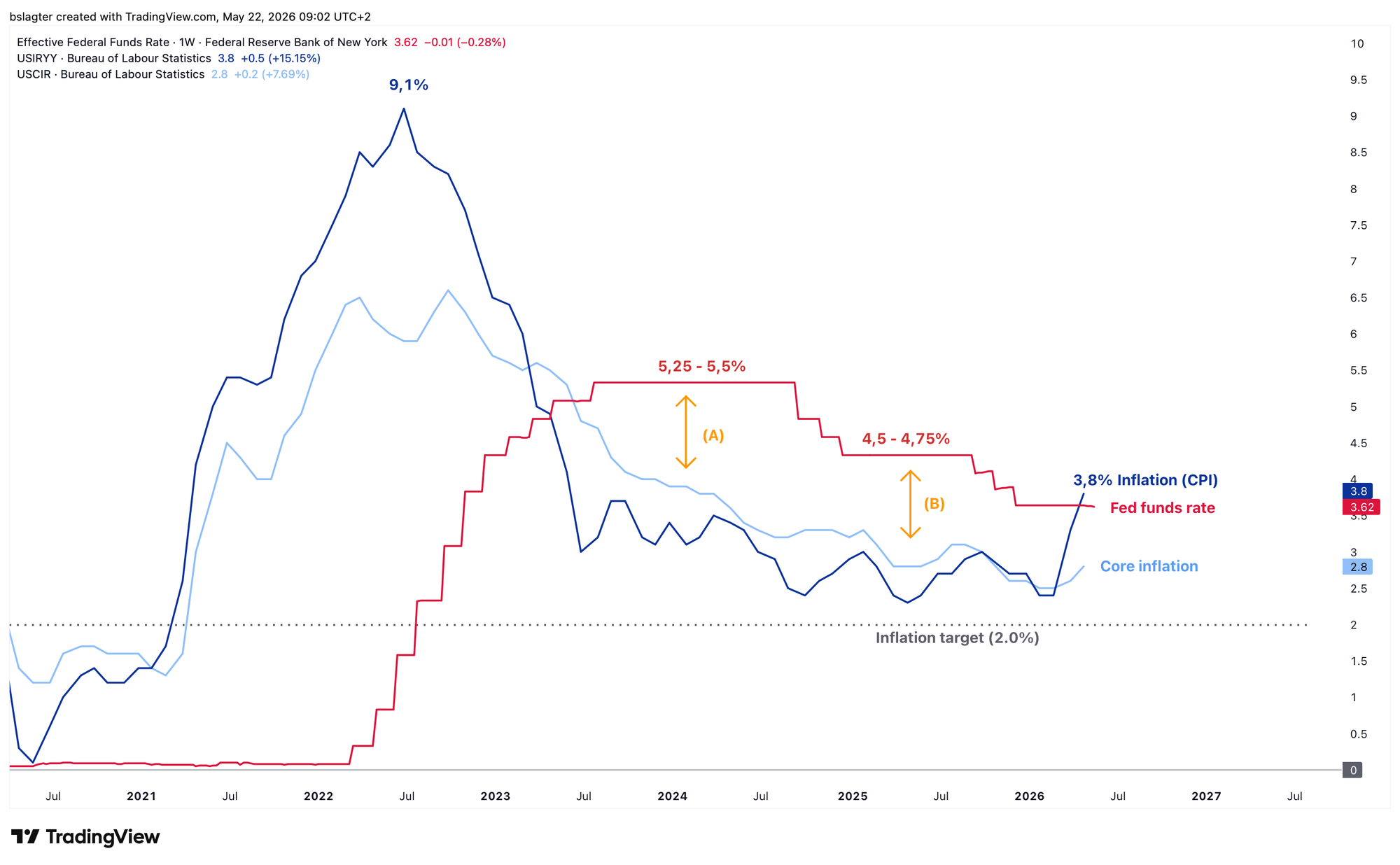

That brings us to the chart below. It shows US CPI inflation (blue) and the policy rate (red). For three years, the rate sat above inflation and declined along with it. This kept the gap between rates and inflation (A) and (B) roughly the same. Recently, inflation rose to 3.8%, above the policy rate which currently sits in the 3.5–3.75% range.

Is hiking the policy rate to 5.5% like in 2022 a solution? That's off the table without causing serious damage. A nudge up or down — those are the options. Until something breaks: in a deep recession, rates can come down sharply, and in an inflation blowout, rates will have to go up sharply.

Policymakers are desperately trying to avoid those scenarios. Soothing speeches, subtle support measures for banks and the bond market, and industrial stimulus are meant to keep the economy on the narrow path between the two cliffs.

That brings us to the question of how long this secular bull market can hold. The chart below shows the S&P 500 adjusted for CPI inflation. The purchasing power of the broad stock index, in other words. We're now 17 years into a bull market.

"Bull markets don't die of old age" is a Wall Street adage. Secular bull markets don't have an expiration date. What typically happens is that certain vulnerabilities build up over the years and suddenly become visible through a combination of circumstances. As you can tell, that can take quite a while if you're lucky.

Predicting the end of a secular bull market is therefore a fool's errand. You're wrong over and over until you're right once. Just like with cyclical bull markets, it's smarter to stay invested until the (secular) handbrake gets pulled.

Right now, that means a portfolio with:

- Equities. With extra attention to tech and the infrastructure needed for AI.

- Real assets. Gold, silver, and bitcoin. Perhaps some commodity ETFs.

Bonds aren't very attractive. They yield less than inflation and the counterparty risk is not negligible.

It's frustrating that bitcoin is lagging behind the stock market. Enough to make you lose heart, you might say. That sentiment fits this phase of the bear market. We're also seeing capitulation, like Mark Cuban selling his bitcoins.

After rain comes sunshine, as the saying goes. After winter comes summer. After low tide comes high tide. And after the bear market comes the bull market.

We need to be patient — the time isn't ripe yet. There's a good chance that a year from now, we'll have left the declining trend on the weekly chart behind. That we'll be back above the 50-week moving average, with a higher high (HH) and higher low (HL) printed on the chart.

Until then, bitcoin is the domain of investors who are building their position with conviction for the long term. A little each week or month. Until all the Mark Cubans of this world have exited, and the next bull market begins.

We continue with the following topics:

- Hyperliquid steals the show

- Bitcoin must fight for capital in the AI era

- Bitcoin feels the pain of the American consumer

1️⃣ Hyperliquid steals the show

Bert

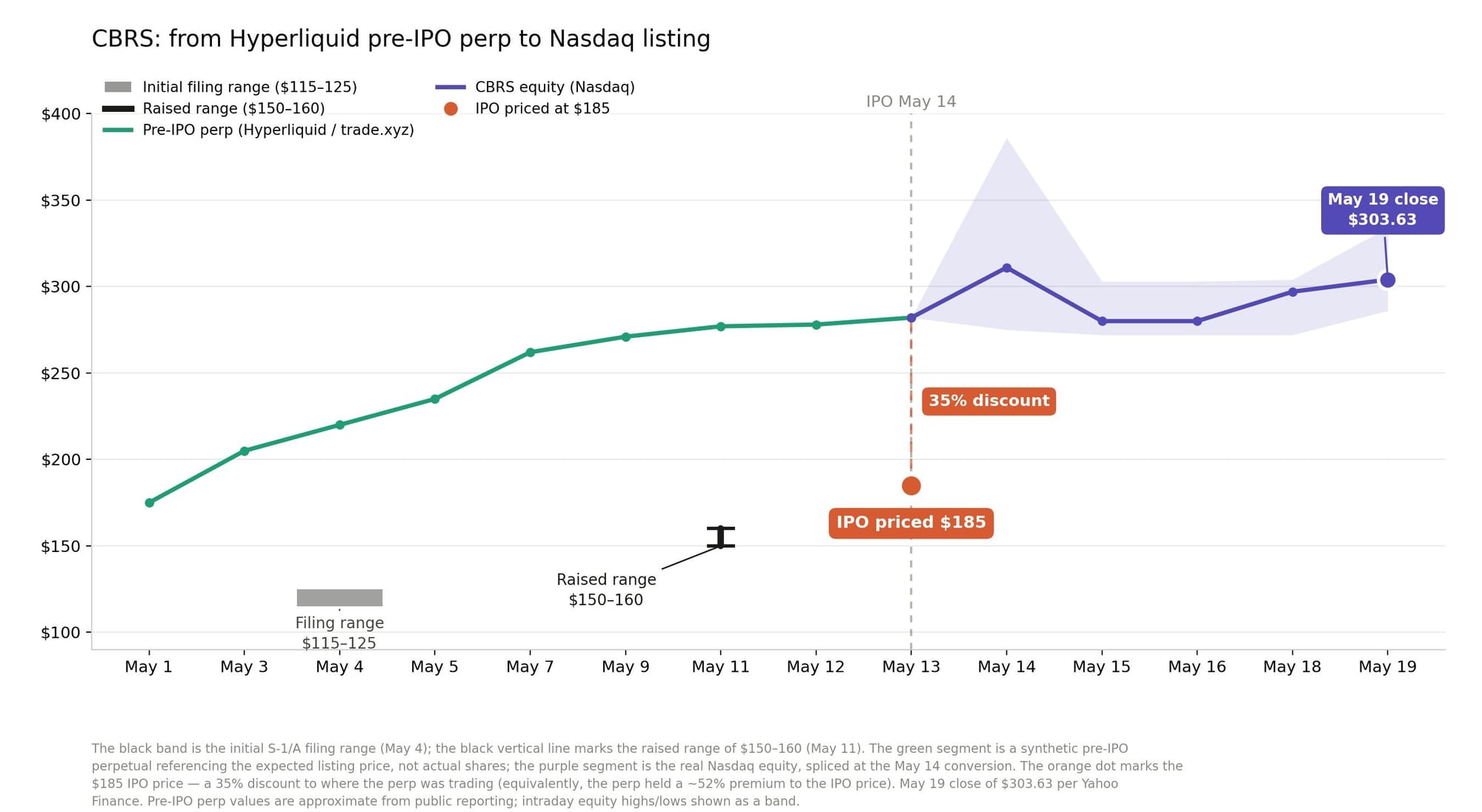

On May 14, Cerebras Systems, which specializes in advanced AI hardware, went public. Ten days earlier, the IPO price was estimated at $115–125, revised on May 11 to $150–160. The IPO priced at $185. The price on the first day of trading? Just under $300.

That means the company could have raised significantly more money. If only they had known there was so much interest in their shares...

David Schamis, CEO of Hyperliquid Strategies, posted the chart below on X, along with a call for SpaceX not to make the same mistake as Cerebras by ignoring the pre-IPO price of its stock on Hyperliquid. There, the Cerebras perp had already been trading around the eventual IPO price for five days.

It's one of the examples where Hyperliquid proves useful, even (or perhaps especially) outside the crypto world. In March, we discussed on Satoshi Radio #407 the attention Hyperliquid was getting for 24/7 trading in perps tracking oil, gold, and stock indices.

That's generating attention. Bitwise CEO Hunter Horsley called Hyperliquid the winner in the 'revenue chains' category. And Bloomberg analyst Eric Balchunas is surprised by the growth of the HYPE ETFs.

Cam Khosravi, analyst at Bitwise, shared the chart below, noting: "roughly 97% accrue back to HYPE holders through automated open-market buybacks."

It's paying off handsomely for HYPE. The price climbed this week to $62.60, just above the previous record of $59.60 set in September.

With a market cap of $15 billion, the token has risen to tenth place on the ranking of largest crypto assets. Solana ($50 billion) and Ethereum ($250 billion) are still considerably larger.

The pre-IPO market could fuel a further catch-up. If Hyperliquid becomes the go-to venue where Wall Street follows the IPOs of SpaceX, OpenAI, and Anthropic, the next leg up could come quickly.

2️⃣ Bitcoin must fight for capital in the AI era

Thom

The rise in global bond yields is currently a widely discussed topic in the financial world. A frequently cited explanation for rising yields is, of course, the war in Iran, which drove oil prices higher and pushed up inflation. That's undoubtedly a factor.

Mike Dolan, a Reuters columnist, offered a different and interesting explanation this week. According to Dolan, the bond market is starting to price in a world where artificial intelligence structurally raises the neutral rate.

The neutral rate is the interest rate level at which the economy is neither being slowed down nor stimulated. In the 2010s, that rate was presumably low, because there was an abundance of savings, productivity growth disappointed, and businesses invested little. That environment made extremely low rates possible.

The AI revolution appears to be changing that. Goldman Sachs estimates, for example, that $7.6 trillion in AI investments will be needed over the next five years.

If companies are scrambling for capital en masse and AI simultaneously boosts productivity, the economy can withstand higher rates. Then the neutral rate is higher than central banks currently assume. In that case, current monetary policy may be less restrictive than it appears on paper.

That explains why stocks and yields can rise simultaneously. Stocks rise because investors expect higher earnings from AI. Bond yields rise because the market is pricing in stronger investment demand, higher potential growth, and persistent inflation.

A structurally higher rate doesn't have to be disastrous for bitcoin. The main problem isn't that ultra-low rates won't return anytime soon, but that the demand for capital has grown enormously. The AI revolution is absorbing massive amounts of money for chips, data centers, energy infrastructure, and commodities. As a result, bitcoin faces more competition in the battle for capital.

That realization may be even more important for the bitcoin price in the short term than the debate about the old era of ultra-low rates. Investors don't just have to decide whether bitcoin is attractive, but also whether it's more attractive than the enormous investment opportunities the AI revolution is offering right now.

Bitcoin is therefore no longer competing solely with government bonds, equities, and gold, but also with a massive AI investment cycle that is drawing capital toward itself and remains the dominant narrative in financial markets for now.

3️⃣ Bitcoin feels the pain of the American consumer

Thom

Bitcoin has historically been an asset primarily driven by retail investors. Although bitcoin has been steadily institutionalizing since the launch of the US ETFs in January 2024, retail still plays a crucial role in price formation.

While US stock indices keep hitting new records almost without interruption, bitcoin is clearly lagging. From the preliminary bottom of $60,000, bitcoin's price has bounced back considerably, but an assault on the all-time high is still a long way off.

Although the prevailing risk appetite in financial markets may result in a relatively shallow bear market for bitcoin, there's no sign of real euphoria.

According to analysts at Market Radar, this has to do with the nature of the AI economy. It functions as a fairly closed system that primarily runs on institutional capital, corporate investment, and the massive balance sheets of hyperscalers.

Bitcoin's underperformance, they argue, is symbolic of the K-shaped economy in the United States. On one side, the AI sector and Wall Street continue to perform exceptionally well. On the other, the American consumer is under increasing pressure from higher prices, rising rates, and expensive financing for mortgages, cars, and credit cards.

On the surface, the market looks risk-on because stock indices and chipmakers are setting new records. Under the hood, however, that risk appetite is primarily coming from the institutional AI chain.

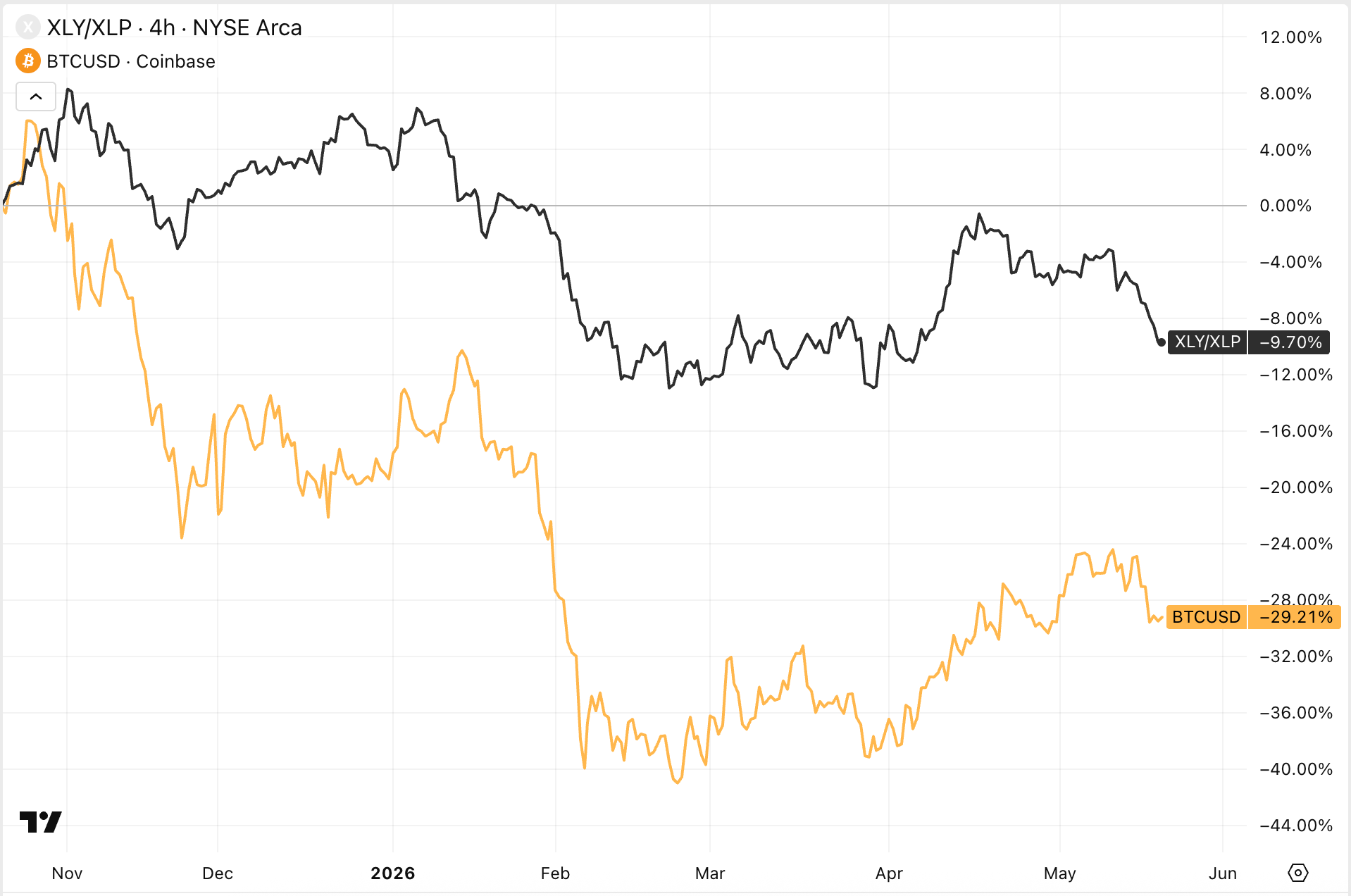

The consumer's struggles are also clearly visible in the chart below. It shows companies that generally sell discretionary products (XLY) versus companies that primarily provide essential goods (XLP).

When consumers have more room for luxury products, XLY tends to rise relative to XLP. Right now, we're seeing the opposite. What stands out is that the price trajectory of this ratio closely mirrors bitcoin's price action since the end of 2025.

This is obviously not the only explanation for bitcoin's underperformance, but it likely plays a role. The American consumer is clearly buckling under developments that are driving higher inflation and rising rates.

At the same time, bitcoin's institutionalization is in full swing. Bitwise's Hunter Horsley recently noted, for example, that last quarter was Bitwise's best ever in terms of institutional capital inflows.

Yet for now, that's still not enough to push bitcoin to a higher level. Retail investors still play an important role in bitcoin's price formation. And we shouldn't forget that AI investments now represent much more competition for bitcoin than during the 2021 cycle.

Retail investors are drawn to hype and quick returns. And unfortunately, bitcoin and crypto are not the place for that right now.

In closing

All previous editions of Alpha Markets can be found in the archive. Questions, comments, and suggestions are always welcome in the community.

Thank you for reading!

To stay informed about the latest market developments and insights, follow our team members on X:

- Bart Mol (@Bart_Mol)

- Peter Slagter (@pesla)

- Bert Slagter (@bslagter)

- Mike Lelieveld (@mlelieveld)

We appreciate your continued support and look forward to bringing you more comprehensive analysis in our next edition.

Until then!