The Monster Under Your Bed

Bitcoin hovers around $66,000—surprisingly stable given this week's chaos: unlawful tariffs, a dystopian AI report rattling markets, and the hunt for scarcity in an age of deflation.

Last Friday, the U.S. Supreme Court ruled that a large portion of the import tariffs Trump imposed last year are unlawful. The court did not rule on how to handle tariffs already paid—that's for lower courts to decide.

Trump was predictably furious and announced new tariffs of first 10% and later 15%. The European Parliament has postponed the vote on the trade deal with the U.S. "Pure tariff chaos from the American government," wrote trade committee chair Bernd Lange on X.

Financial markets weren't fazed. Last year, every tariff rumor caused wild swings—now investors just shrug it off. There are bigger fish to fry, like AI.

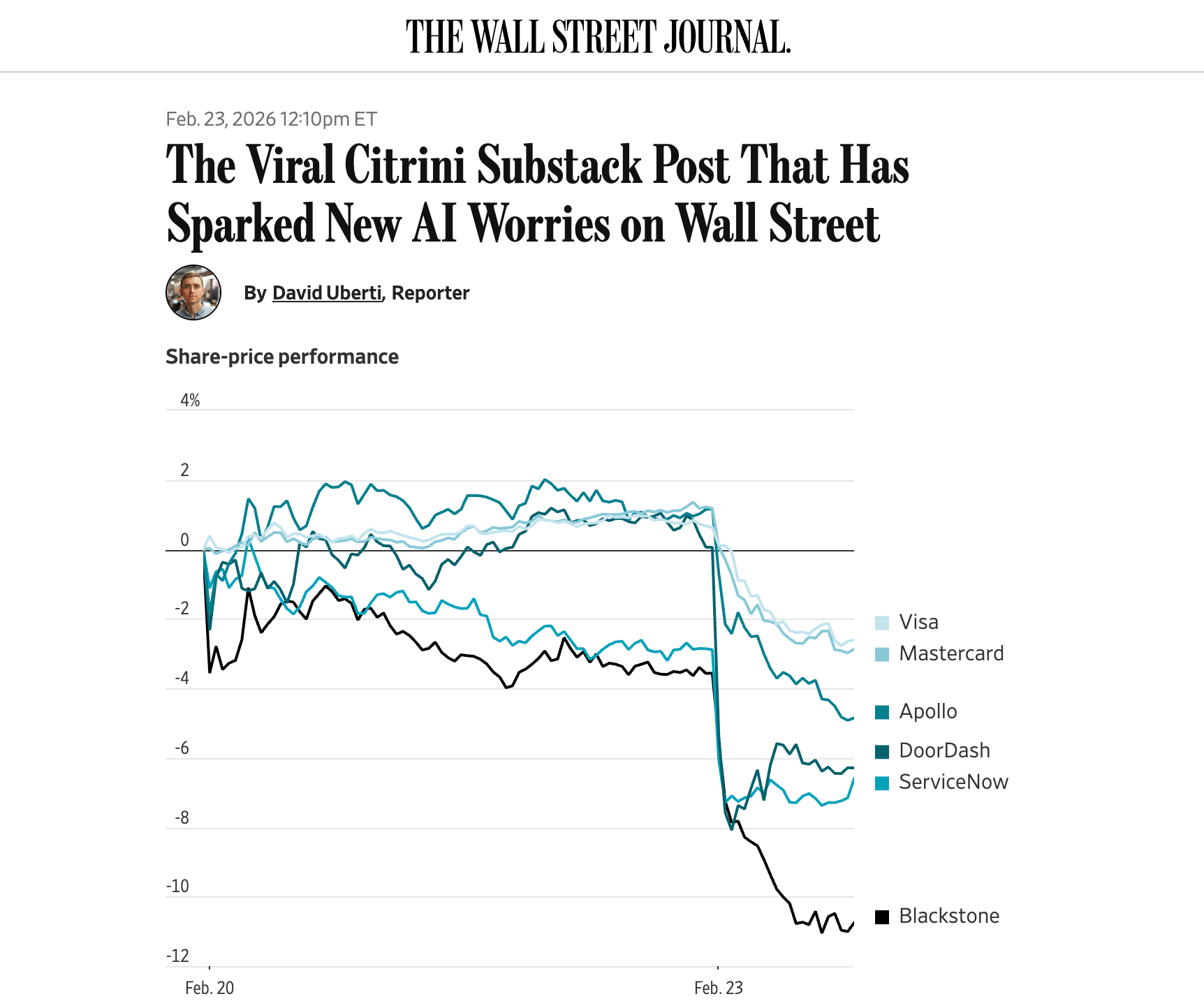

On Sunday, February 22, analysts at Citrini Research published the report The 2028 Global Intelligence Crisis. It outlines a scenario where AI continues improving at the same pace, dragging industry after industry into a downward spiral. After a peak in late 2026, stocks plunge into a deep bear market.

The report struck a nerve. Various stocks tumbled on Monday. The FD described it in an article headlined "Report with 'dystopian' AI scenario sends investors into panic."

It's important to keep a cool head. Just because there might be a monster under your bed doesn't mean there actually is one.

You could say there are three archetypal scenarios for AI over the next three years:

- The utopian scenario: AI disrupts the world, bringing widespread abundance and prosperity. A period of massive economic growth. Some people lose their jobs, but new ones emerge. Schumpeter & creative destruction.

- The doom scenario: AI disrupts the world, causing widespread damage. Companies go bankrupt and many people become unemployed. Every business gets squeezed and must scale up or collapse.

- The skeptical scenario: AI can do far less than people believe. Its capabilities are overhyped. It's a much slower 10+ year process where AI gradually provides more support.

Arguments can be made for all three. And because the consequences could be so significant, it's worth considering all of them. But the doom scenario being imminent is far from certain.

Jordi Visser, author of Bitcoin's Silent IPO, appeared this week on The Pomp Podcast and discussed companies getting hammered by AI. He explained it as 'multiple compression': those companies will still make profits this year and next, but what about three, four, five years from now? The uncertainty justifies a lower multiple, and therefore a lower stock price.

The Citrini report describes a variant of scenario 2. And the market has been pricing in scenario 2 over recent months. The software ETF IGV has fallen 35% since October, two-thirds of that in the past two months. Is that justified?

Yesterday, Jack Dorsey, CEO of fintech Block, announced that the company is laying off 40% of its 10,000 employees. Not because the company is struggling—quite the opposite. The departing employees are receiving generous packages and dignified farewells.

According to Dorsey, AI tools allow the organization to restructure. Smaller teams, a flatter organizational structure. Dorsey is taking the pain all at once, rather than slicing off a piece every few months.

This could be an argument for scenario 1. Companies reinventing themselves, focusing on what their customers (and their customers' AIs) can't easily do themselves. The stock jumped more than 20% after-hours on the announcement. Investors apparently think it's the right direction at first glance.

Monsters under your bed. Or burglars behind the curtain. As a child, these things could really send you into a panic. The nice thing was that you could easily resolve the uncertainty about whether danger was present by simply turning on the light.

For negative scenarios in financial markets, it's different. Only time can reveal which doomsday stories come true and which don't. Is quantum computing really a major threat? Is the 'digital gold' narrative truly dead? Will AI plunge the world into a deep recession in the coming years?

The skeptic will express doubt about any extreme scenario, suggesting things won't go that far. But history is shaped by black swans: something improbable that happened anyway, or something probable that didn't.

Life is the cumulative effect of a handful of significant shocks; this is easy to see. It's also not difficult to examine, from your armchair (or barstool), how large a role Black Swans play.

Try this exercise. Take stock of your own existence and count the significant events, the technological changes, and the inventions that have occurred in our world since your birth, and compare them to expectations beforehand. How many were foreseen? Look at your personal life, your career choice, how you met your partner, your exile from your country of origin, the times you were betrayed, the moments when your financial situation suddenly improved or worsened. How often did these things happen according to plan?

(Nassim Taleb, The Black Swan)

In conversation with Pompliano, Jordi Visser arrived at the hypothesis that all stocks are becoming susceptible to deflation, resulting in price declines due to uncertainty about future profits. "I don't know what will be around in three years," he said about companies and their stocks.

He concluded that a search for scarcity is the logical consequence—something that can't be replicated by a swarm of AI agents. "Avoid things that are being deflated," and you're not left with much. Visser suspects bitcoin is in its element there.

According to Visser, the turning point will be recognizable by bitcoin decoupling from software stocks. For now, they still move closely together, as you can see in the chart below.

We haven't seen relative strength from bitcoin since early summer 2025. Even when bitcoin hit new all-time highs in August and October, it was less impressive than many other investments.

A reversal of bitcoin's downtrend relative to other investments—like tech stocks, gold, or the software ETF—would signal that we're nearing the end of the bear market.

We continue with the following topics for our Alpha Plus members:

- The AI hype has cooled off

- The weekly cycle

- Is ether stepping out of bitcoin's shadow?

- Is the U.S. economy more vulnerable than expected?

1️⃣ The AI hype has cooled off

Thom

Bitcoin needs a high degree of risk appetite to thrive. Since Q4 2025, that's clearly been absent, and we've seen the bitcoin price drop over 50% from its all-time high.

Investors' cautious stance was also evident after Nvidia published its quarterly results on Wednesday. Although those numbers beat expectations on virtually every front, Wall Street didn't respond enthusiastically. But there's also no decidedly negative investment climate.

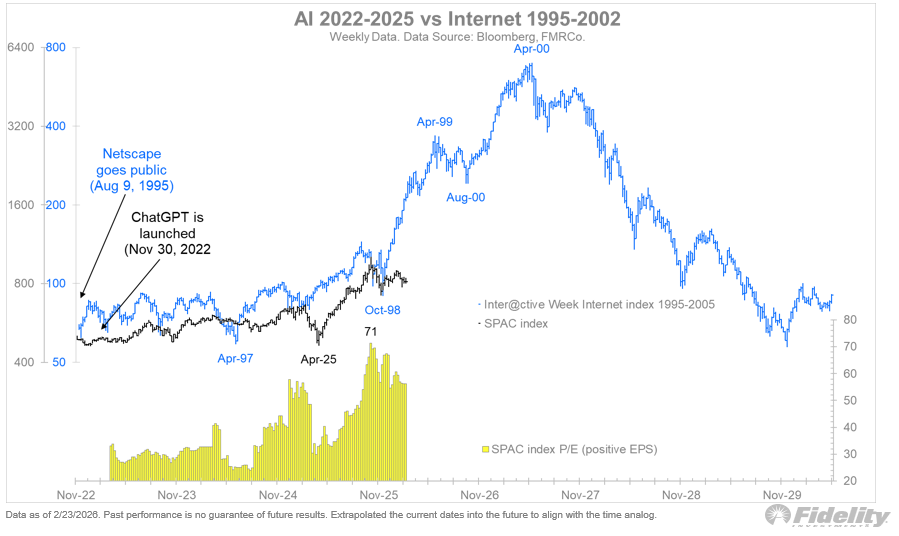

The following series of charts from Jurrien Timmer, macro analyst at Fidelity, captures the current landscape nicely in my view.

The first chart shows the speculative SPAC index, which has mostly traded sideways since peaking in late 2025. Timmer overlaid the dotcom bubble as a reference, noting: "In October, the question was whether the AI boom was turning into a bubble. Today, that question feels like a distant memory."

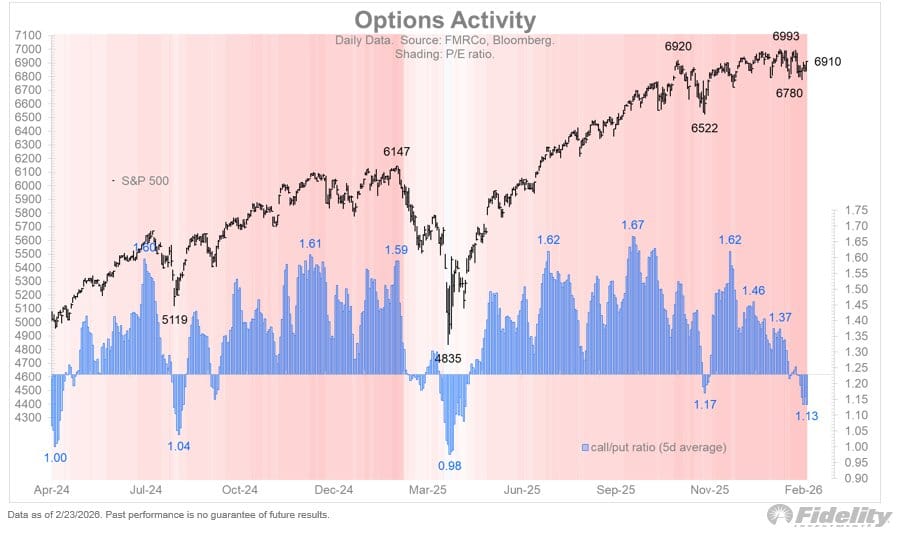

The absence of speculative frenzy is also reflected in the call/put ratio. At 1.13, it's around the level we typically see near local market bottoms.

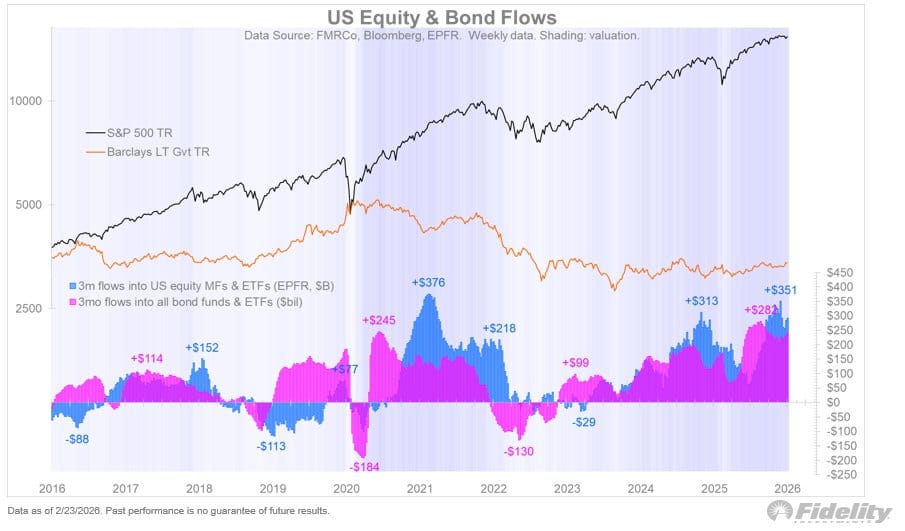

While we're not in a market phase where speculative investments perform well, we still see robust capital flows into both stocks and bonds, as shown in the final chart.

This series of charts essentially says: the market isn't overheated, the AI hype has cooled, true speculation and risk appetite are missing, but there's no widespread panic, mass flight to cash, or systemic stress either. The truth lies somewhere in the middle, or perhaps just above it.

We're in a global bull market, but one that's not as pronounced and explosive as what we saw in 2021. That's probably what's holding bitcoin back, but this also supports the idea that a deep bear market is unlikely.

2️⃣ The weekly cycle

Bert

We're in week 14 of this weekly cycle. If it lasts around 30 weeks like previous weekly cycles, we're roughly halfway through.

There's a good chance the $98,000 in week 8 was the top of this weekly cycle. A bear market rally could still emerge, but the odds of it exceeding $98,000 are slim.

This weekly cycle has 'failed,' meaning the price has dropped below its starting point. That's normal in this phase of the market cycle. The last one or two weekly cycles of a yearly cycle are typically declining.

If this week's close is below $67,600, we'll mark the sixth consecutive red week. That doesn't happen often. In 2022, we saw nine red weeks in a row during a similar bear market phase.

From a cycle analysis perspective, the most likely scenario remains that we'll hit a weekly cycle low (ICL) somewhere toward the end of Q2. There's a real chance that will also be the bear market bottom.

3️⃣ Is ether stepping out of bitcoin's shadow?

Sam

Last Wednesday was an old-fashioned green day for crypto investors. They weren't exactly the 'omega candles' we were promised during the bull market, but more than fine given current market conditions.

Our base case is that this rally is a bear market rally that will eventually stall, with a visit to $60,000 or lower to follow. That doesn't mean this rally is already over. A bear market rally can be quite aggressive, with sharp gains in a short time.

If we assume this recent strength continues and we want to capitalize on it, it might be worth focusing on ether rather than bitcoin.

To measure the relationship between these two, we look at the ETHBTC trading pair on the chart. When it's rising, ether (ETH) is stronger; when it's falling, bitcoin (BTC) is stronger.

Let's examine this chart along with the arguments for why ether is showing signs of relative strength. In the image below, the white arrows show how the blue line has played an important role since 2021. It consistently produced strong reactions as both support and resistance.

The daily chart also shows that the blue line has been significant resistance since early February. Whenever there was a daily close above it, the price was pushed back below the next day. Wednesday saw a strong close above it, but unlike previous times, Thursday held it as support.

If ether stays above the blue line in the coming days, it's likely that ether will outperform bitcoin in the near term. It's important to note that the ETHBTC chart can also rise when both bitcoin and ether are falling. In that case, ether simply falls less.

4️⃣ Is the U.S. economy more vulnerable than expected?

Thom

The U.S. economy grew just 1.4% in Q4. That was well below many analysts' expectations. For many, this figure came as quite a negative surprise—but not for those viewing the economy through the lens of EPB Research's 'Cyclical GDP' theory.

According to EPB Research, much economic analysis wrongly focuses on total growth, consumption, or the labor market. We hear things like "the consumer is strong" or "America is a services economy."

That's partly true, since personal consumption accounts for about 70% of U.S. GDP. But the largest portion of that—services—is very stable and barely responds to rate hikes.

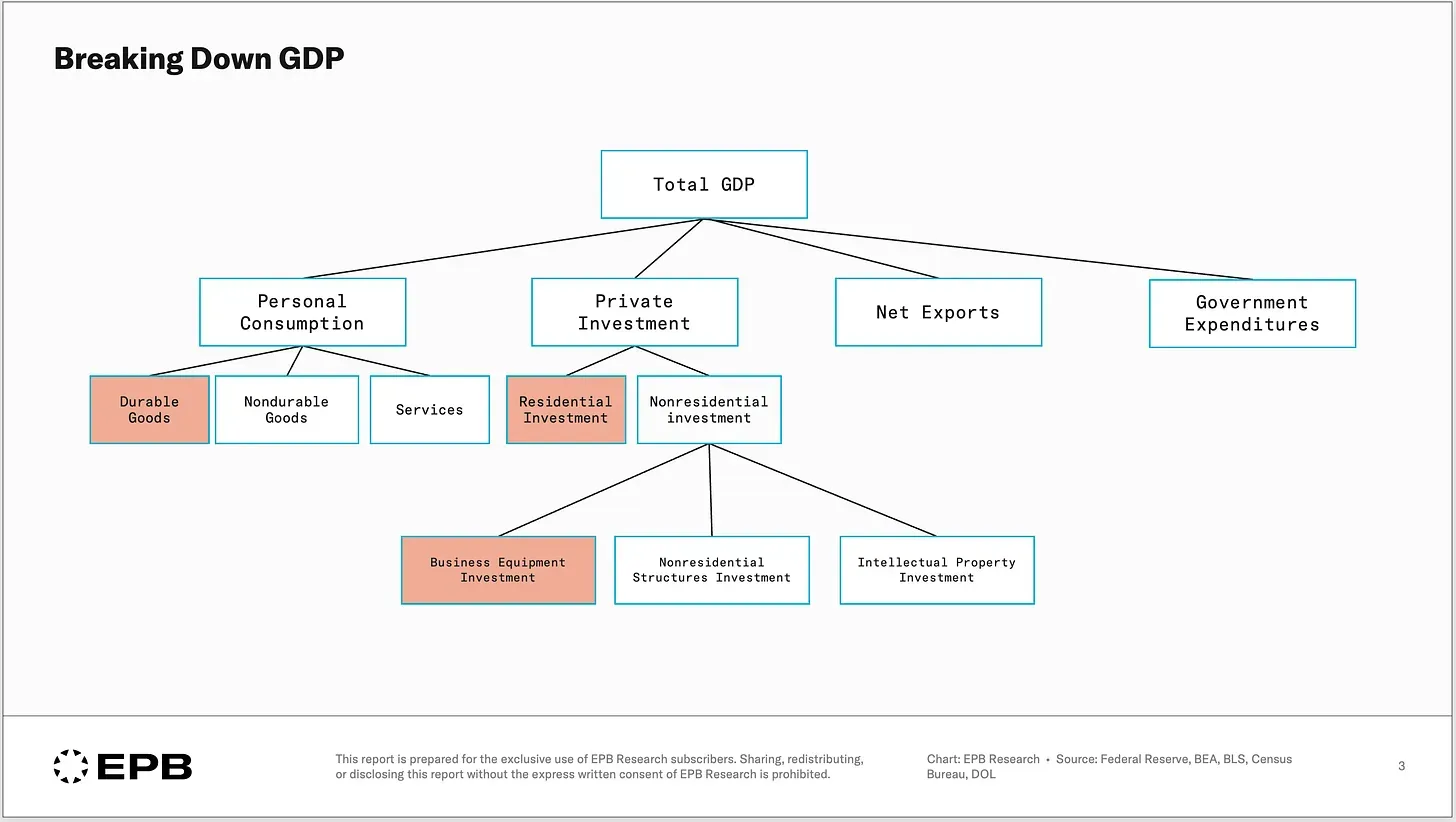

The real swings in the economic cycle, according to EPB Research's theory, come from just three categories within the overall GDP umbrella:

- Durable consumer goods – like cars and furniture

- Residential investment – housing construction

- Business investment in equipment

Together, these categories make up what EPB calls the cyclical portion of GDP. These components represent about 20% of the economy but have historically been responsible for all recessions.

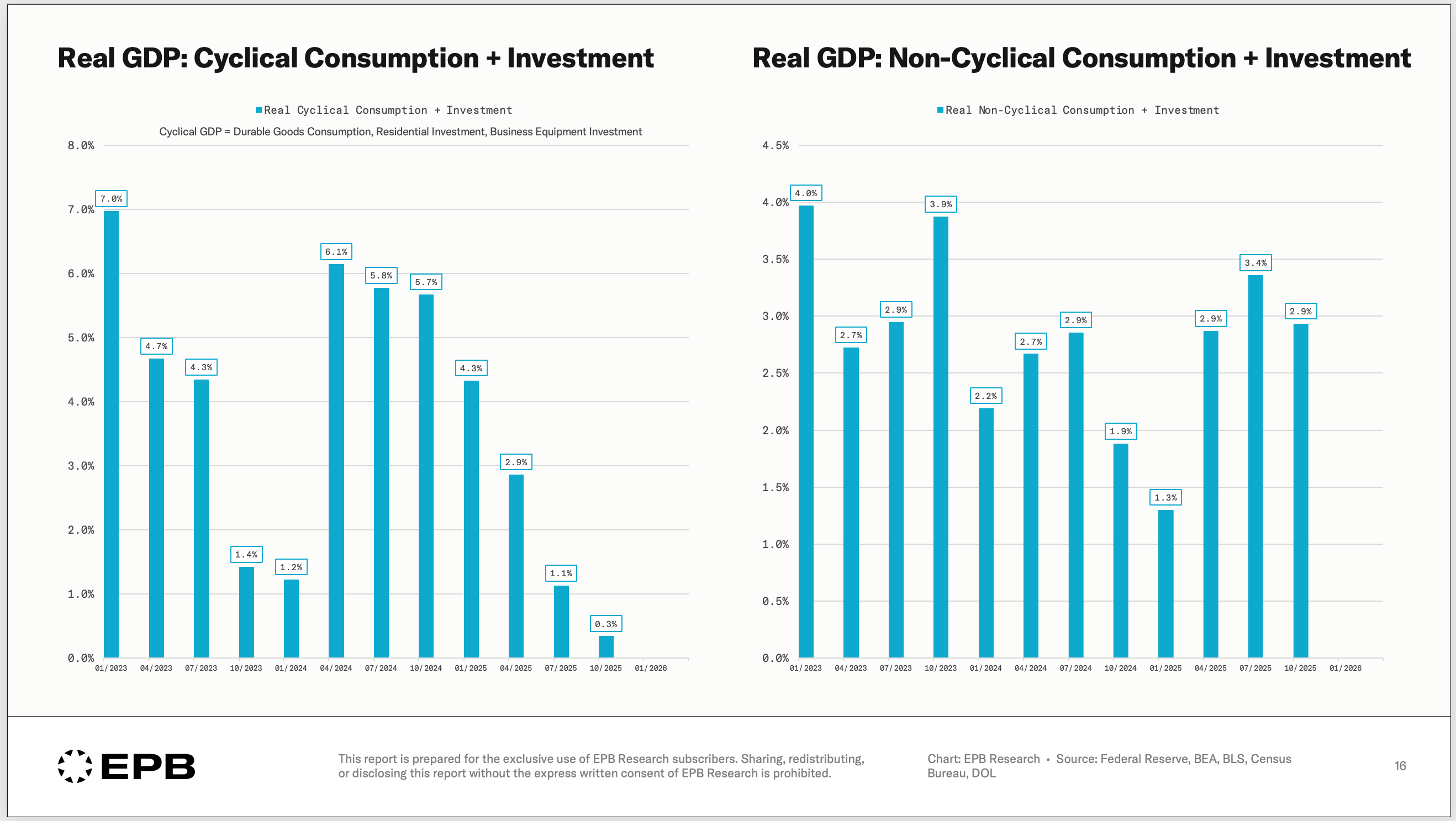

The chart below shows economic growth for the cyclical (left) and non-cyclical (right) portions of the economy over the past 12 quarters.

The non-cyclical portion grew 2.9%—a solid result. The cyclical portion tells a different story. Unlike the non-cyclical part, it IS sensitive to higher interest rates.

In Q4 2025, EPB Research saw the cyclical portion of GDP grow just 0.3%, while it was around 6% a year and a half earlier. The slowdown since then has been sharp and swift.

It appears higher rates are now really starting to bite in that part of the economy. Housing construction and durable consumer goods even showed contraction on average over the past four quarters.

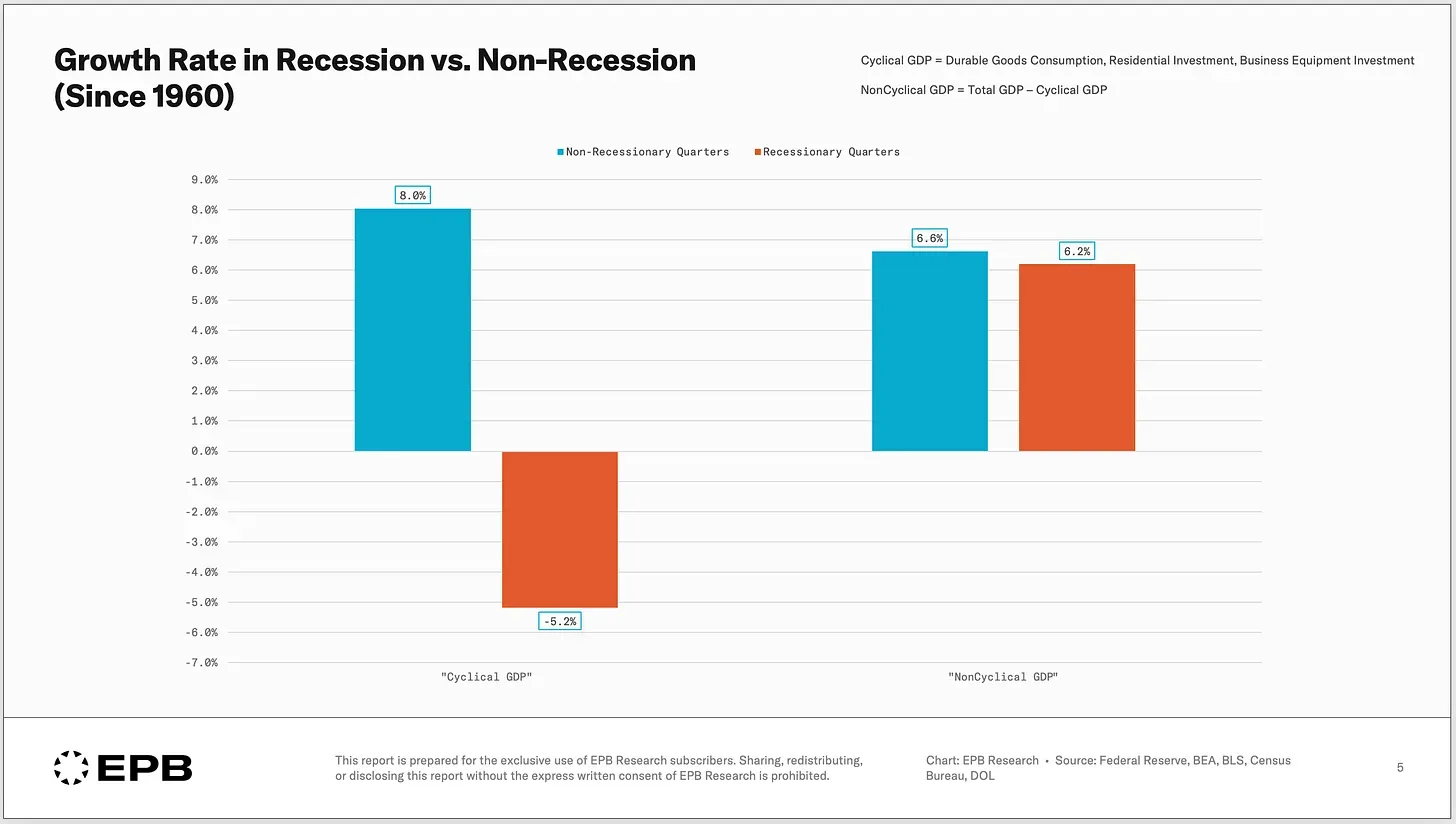

That the cyclical portion provides the signal while the non-cyclical portion is mostly noise is most evident in the final chart. While the cyclical portion grows strongly during non-recessionary periods and contracts during recessions, the non-cyclical portion always grows—even during recessions.

This may not come as a huge surprise, but what seems to have prevented a recession over the past two years was the strong rise in business investment in equipment—in other words, the AI narrative.

Massive investments in data centers, chips, and IT infrastructure have partially offset declines in housing construction and durable consumption. Now that growth in other cyclical segments is flattening and parts of industry are starting to cut jobs, the economy is becoming increasingly dependent on a single engine. And that's a vulnerable position.

This doesn't mean we're necessarily heading for disaster. Positive economic growth continues. However, this may partly explain why extreme risk appetite among investors has diminished—exactly the type of capital flow bitcoin typically needs to rally strongly.

In closing

All previous editions of Alpha Markets can be found in the archive. Questions, comments, and suggestions are always welcome in the community.

Thank you for reading!

To stay informed about the latest market developments and insights, follow our team members on X:

- Bart Mol (@Bart_Mol)

- Peter Slagter (@pesla)

- Bert Slagter (@bslagter)

- Mike Lelieveld (@mlelieveld)

We appreciate your continued support and look forward to bringing you more comprehensive analysis in our next edition.

Until then!