Rising Rates as a Wrecking Ball

Bond yields keep climbing, putting financial markets under severe pressure. Without a swift resolution to the Iran conflict, a deep recession and equity bear market look increasingly unavoidable.

The US central bank normally isn't too worried about inflation that's a direct result of high oil and gas prices. Such an energy shock causes a one-time increase in the price level, Jerome Powell said last week after the rate-setting meeting. The Fed generally looks through that, as long as long-term inflation expectations remain anchored.

It's precisely that condition where the danger lies for the Fed. Inflation has been running above the 2% target for five years now. That's the result of a succession of shocks: the pandemic, the war in Ukraine, import tariffs, and now the war in Iran. Each of those shocks individually has a temporary effect on prices and can't be undone with monetary policy. But because the price increases overlap, together they create stubbornly elevated inflation.

This can cause households and businesses to start expecting permanently higher inflation. Workers then demand higher wages and companies preemptively raise their prices. Inflation thus threatens to become self-reinforcing. Inflation expectations become unanchored. And that's exactly what the Fed wants to prevent, even at the expense of economic growth.

The Fed is increasingly caught between its two mandates: stable prices and low unemployment. For the labor market, it wouldn't be unreasonable to lower rates a bit further and give the economy a boost. But the upside risks to inflation are holding the Fed back.

The market knows this.

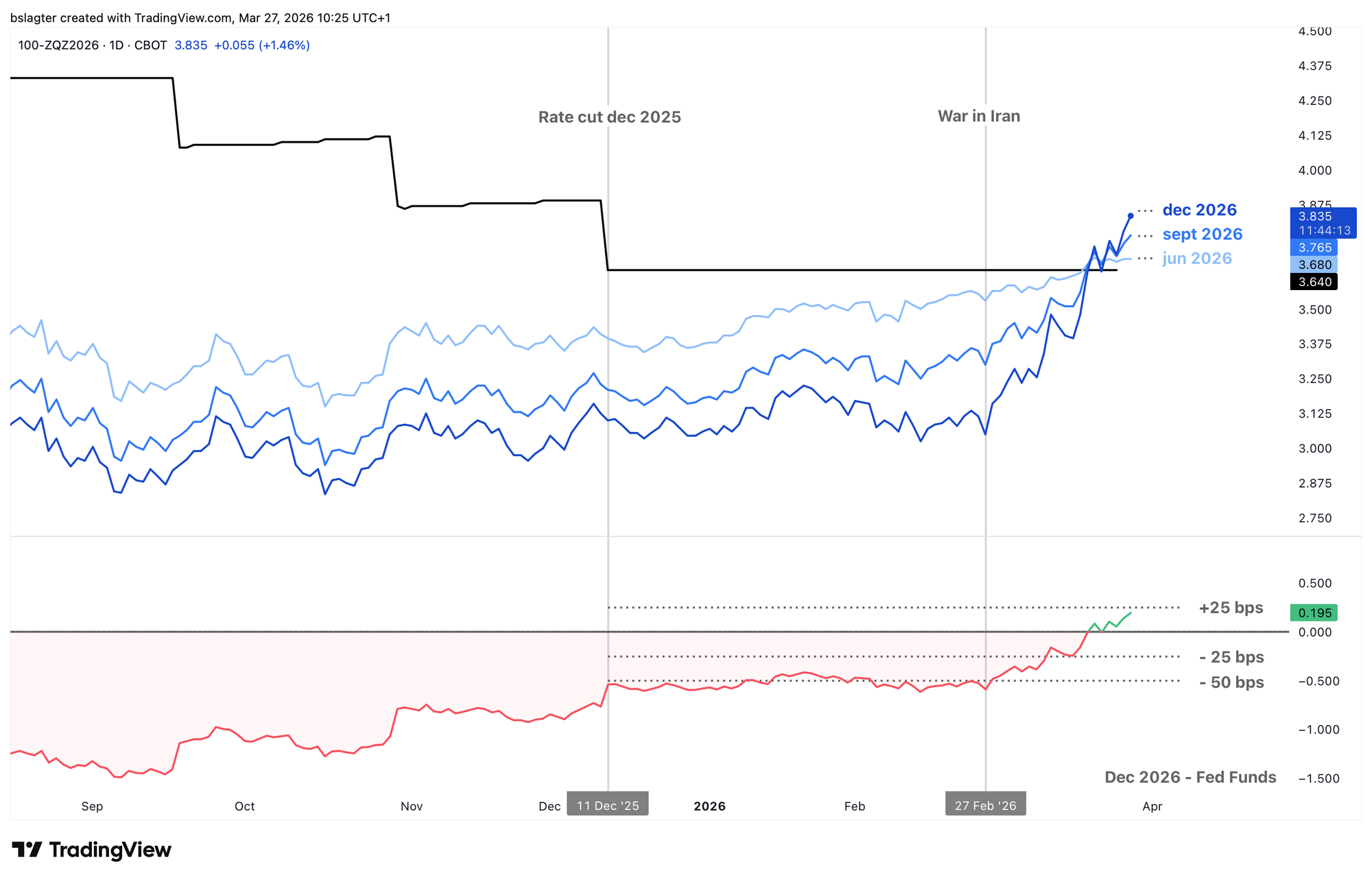

At the start of 2026, the market expected the Fed to cut rates twice this year, bringing the policy rate to 3.0%–3.25%. The dark blue line in the chart below shows the rate the futures market is pricing in for December of this year.

After the outbreak of the war in Iran, that line started to rise. On March 18 and 19, around Powell's press conference, rate expectations made a sharp jump higher. No rate cuts at all this year, was the market's conclusion. By now, a first rate hike has even been priced in.

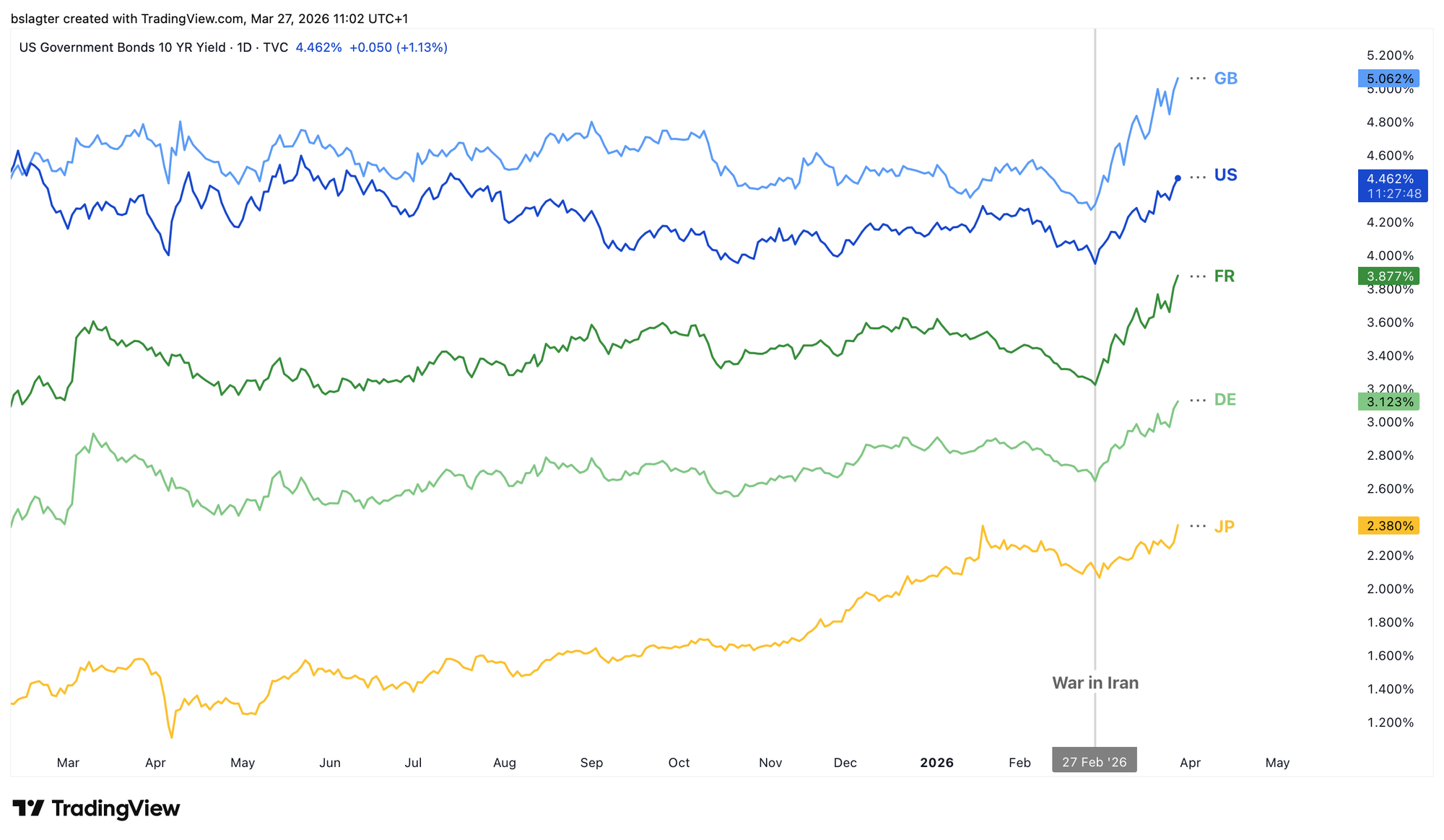

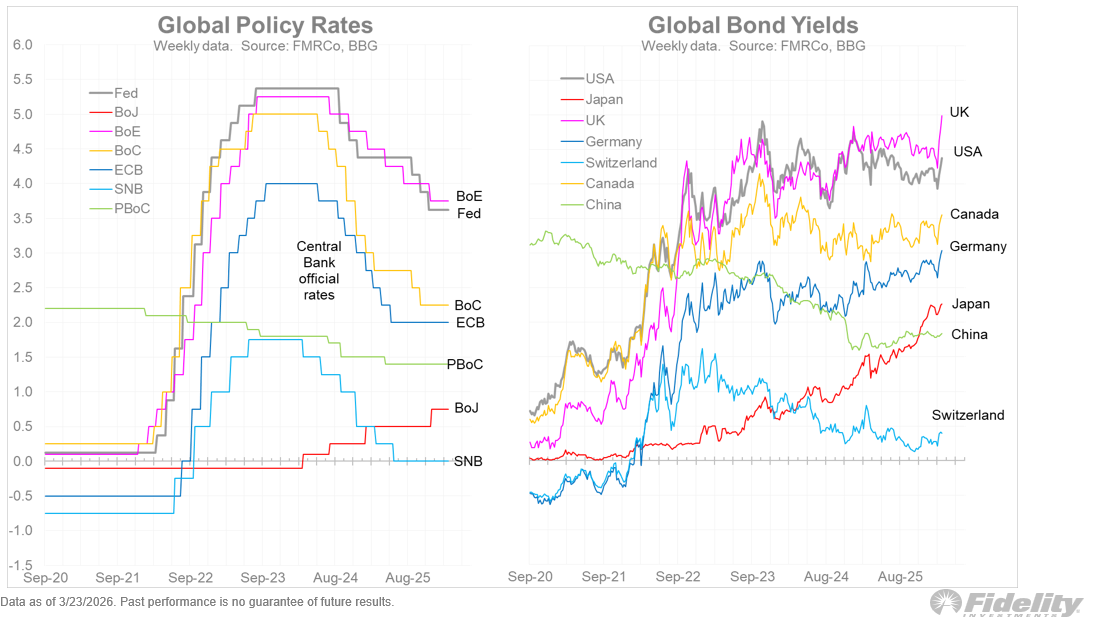

Short-term bond yields move in line with the (expected) policy rate. Long-term yields incorporate expectations about future policy rates and inflation, plus a country-specific risk premium. That premium rises as debt, deficits, and political uncertainty increase. This is a key reason why French 10-year yields typically trade above German Bunds.

The war in Iran is pushing those long-term yields higher as well. The chart below shows 10-year yields for the US, UK, France, Germany, and Japan. On average, they've risen by roughly 0.5 percentage points.

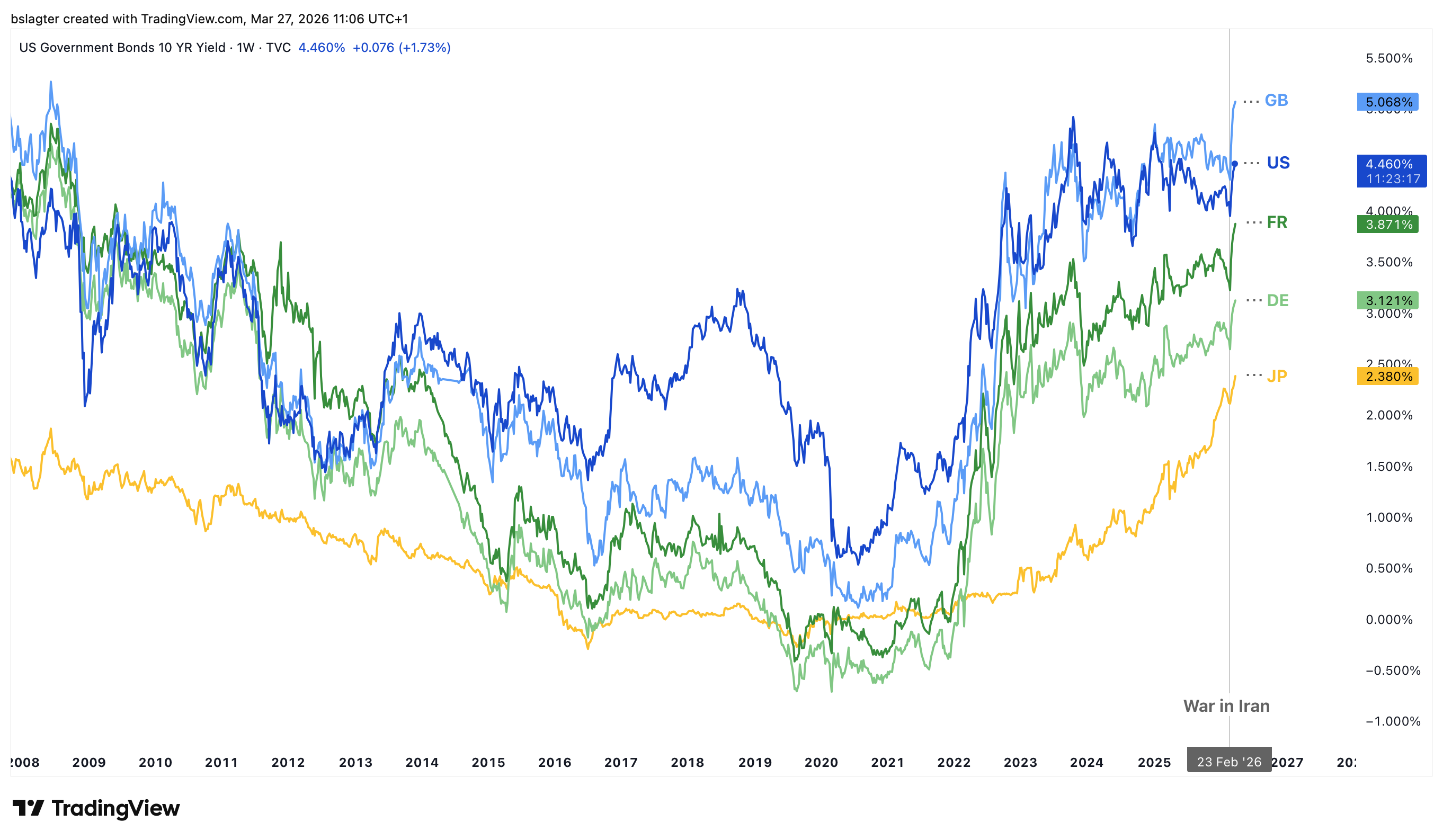

In many countries, long-term yields are now at their highest levels since 2008–2009, while government debt has surged dramatically since then.

When the UK 10-year yield stood at 5% in 2008, government debt was £600 billion, about 40% of GDP. Now that debt has ballooned to £2,900 billion, nearly 100% of GDP. The same yield therefore creates a far heavier interest burden today.

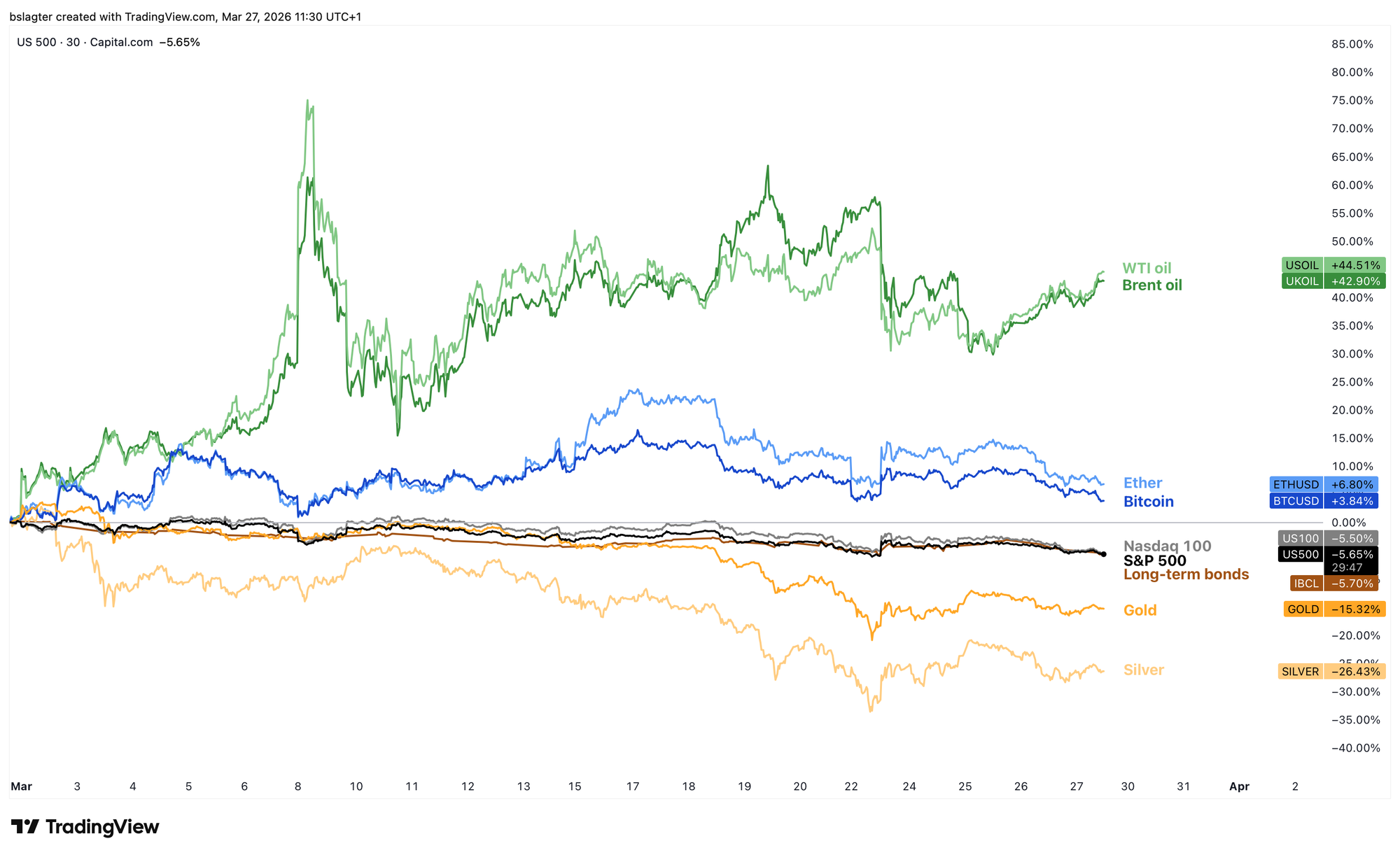

When yields rise, bond prices fall. Higher rates are also a headwind for stocks, as borrowing becomes more expensive for companies and consumer spending takes a hit. Gold is sensitive to real rates. When they rise, gold becomes somewhat less attractive as a store of value.

This fits with the market moves of the past four weeks. Stocks, bonds, and precious metals down. Oil up. Only the crypto market continues to hold up better than you'd expect given the circumstances.

We continue with the following topics for our Alpha Plus members:

- Hanging by a thread

- Daily cycle low approaching for bitcoin

- The Trump pump and its (limited) impact on bitcoin

- Should the Fed intervene?

- Rates are rising — so why is the S&P 500 holding up?

1️⃣ Hanging by a thread

Bert

Financial markets have already priced in the consequences of a modest inflation wave. Somewhat higher rates and somewhat higher energy costs. But a prolonged, global energy crisis is not priced in. The deep recession that would inevitably follow would send stock prices much lower.

So far, the prevailing belief is that the conflict will end quickly. The importance of adequate oil supply is so great that the rest of the world will naturally ramp up pressure to reopen the Strait of Hormuz — or so the thinking goes.

That assumption is now wobbling. Stock markets are teetering on the edge of a cliff. They've declined to their dominant moving average. A weekly and monthly close below this level would signal a transition to a downtrend.

The chart below illustrates this for the S&P 500. The last straw for the bulls is a test of 6,150 as support. But after a weekly close below the 50-week moving average, the scenario of sliding into a bear market becomes increasingly likely.

The Nasdaq 100 appears to have already given up hope. The 40-week moving average plays a bigger role for the tech index than the 50-week average. And we're now sitting well below it.

Only a convincing turn in the war can prevent a (deep) bear market from becoming the primary scenario. A breakthrough that credibly reopens the Strait of Hormuz, allowing the flow of oil, gas, and commodities to resume unimpeded.

We have no indications that such a breakthrough is imminent. One thing is clear: Trump won't be able to talk his way out of this one with posts on Truth Social.

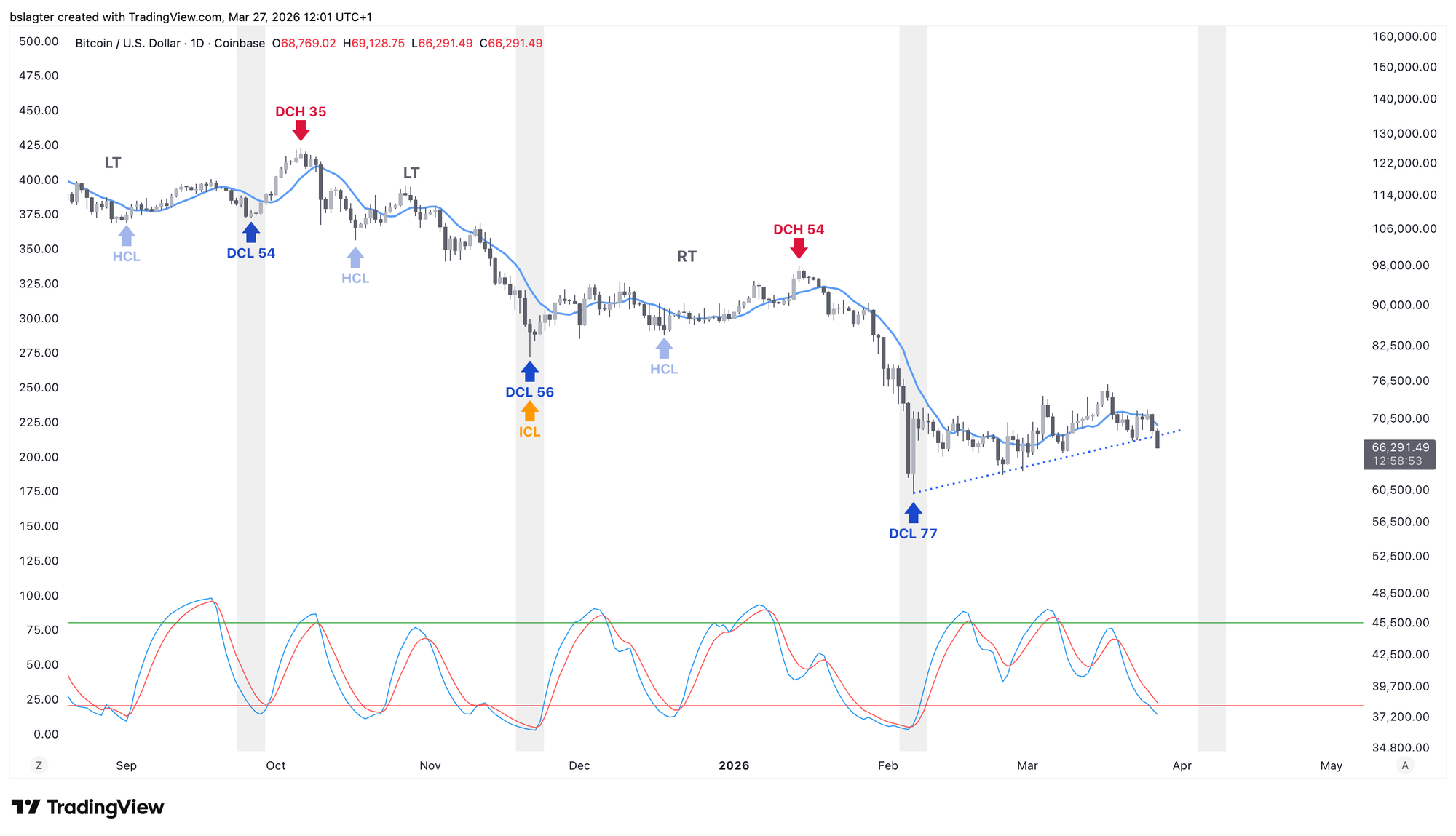

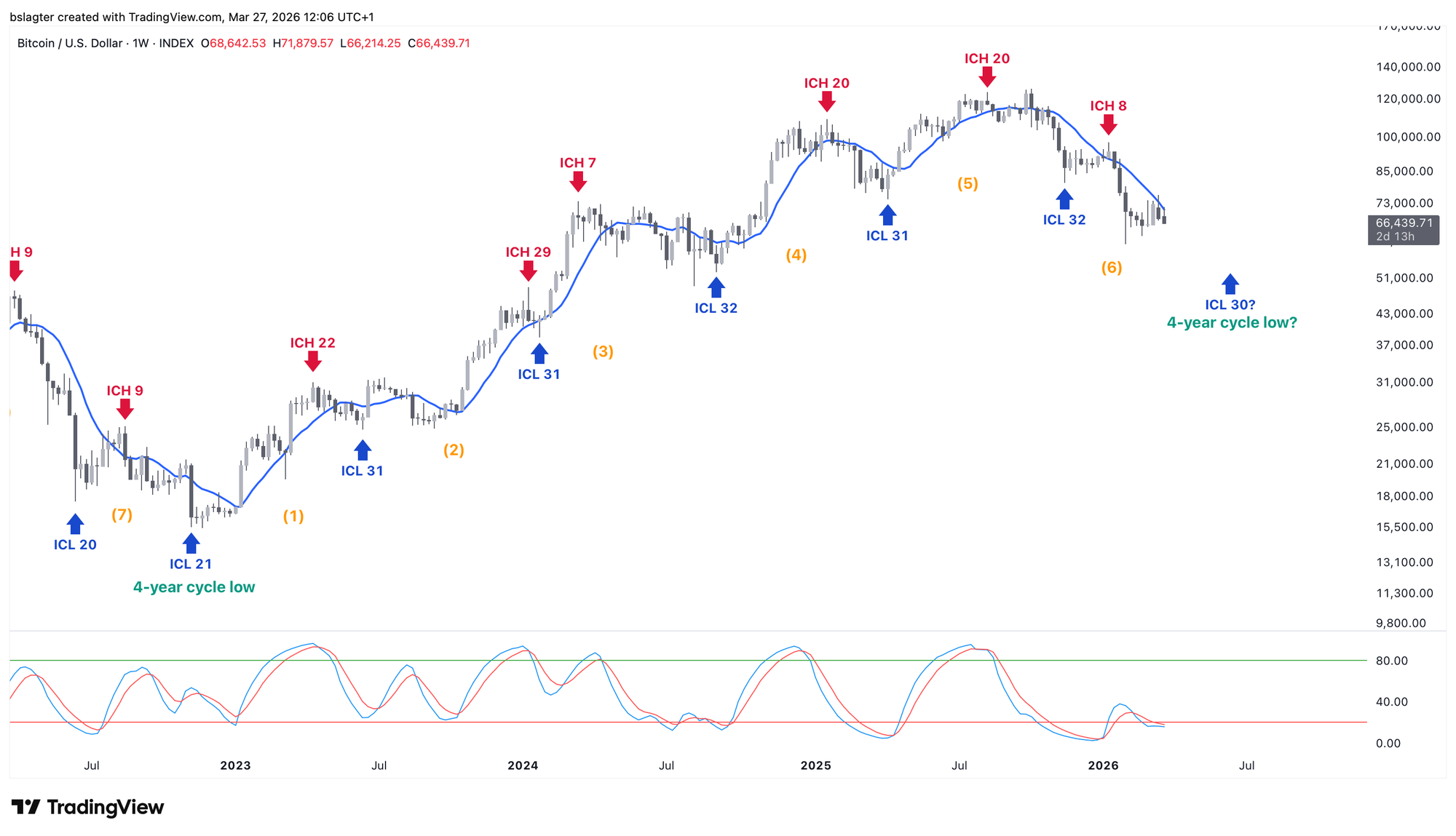

2️⃣ Daily cycle low approaching for bitcoin

Bert

On bitcoin's daily chart, we've been watching the bear flag that has been forming over the past two months. This pattern typically breaks to the downside. And that appears to be happening today.

The timing is perfect for a move toward the daily cycle low sometime in the next two weeks. We're now on day 49 of an average 60-day cycle. This daily cycle could well be shorter than average, since the previous one ran unusually long at 77 days.

The price level at which the daily cycle low (DCL) lands gives us valuable information. Do we stay above $60k? Then this zone between $60k and $75k gains significance. The probability then increases that the bear market bottom won't be much lower.

The first opportunity for such a bear market bottom, through the lens of cycle analysis, is the next weekly cycle low (ICL). We expect that around the end of the second quarter. Until then, the expectation is that we'll see prices lower than the $60,000 level from February 5.

Technical analysis and on-chain indicators suggest that the ultimate bottom doesn't need to be much lower. The $48,000–$60,000 range contains many price targets, with a strong cluster around $55,000.

That's no guarantee it will hold there, but it's also far from certain that this bear market needs to drop below $30,000 for a bottom — comparable to the 77% decline of the previous bear market.

3️⃣ The Trump pump and its (limited) impact on bitcoin

Sam

Last Friday, US stock markets closed in the red. Since markets are closed on weekends and a war was raging with no signs of easing at the time, it's no surprise that investors reduced their risk exposure on Friday evening.

Bitcoin doesn't take days off, and there's an argument to be made that this was one reason bitcoin held up better on Friday, March 20.

Over the weekend, the White House issued Iran a 48-hour ultimatum, which would have meant a serious escalation of the conflict. Iran poured fuel on the fire by threatening to attack the energy infrastructure of surrounding countries.

Bitcoin did react negatively to that, and since the ultimatum was set to expire Tuesday night European time, markets were cautious on Monday morning.

And then it happened. Trump posted on Truth Social that he was extending the deadline, noting that productive talks with Iran about de-escalation were underway. Prices surged. Reports of insiders profiting handsomely quickly followed.

A few days later, we can conclude that, when we zoom out, not much has actually changed. The chart below shows that bitcoin is still trading within the range of roughly $72,000 to $60,000.

As long as bitcoin fails to break above $72,000 and hold, there's a strong chance the price will test the lower end of this range in the near future.

The base case remains that this is an upward correction within a downtrend. In the short term, the price could still move significantly higher if bitcoin does manage to break above $72,000, but the expectation is that a lower high will be set at some point, followed by a return toward $60,000.

4️⃣ Should the Fed intervene?

Thom

This week I came across an interesting piece by Eric Wallerstein, a macro strategist at an asset management firm, arguing that the Fed may need to intervene because of the war in Iran.

In this case, he's not talking about the rate hike versus rate cut debate, but about the US Treasury market. According to Wallerstein, the Fed shouldn't wait and see — it should actively intervene to prevent greater damage.

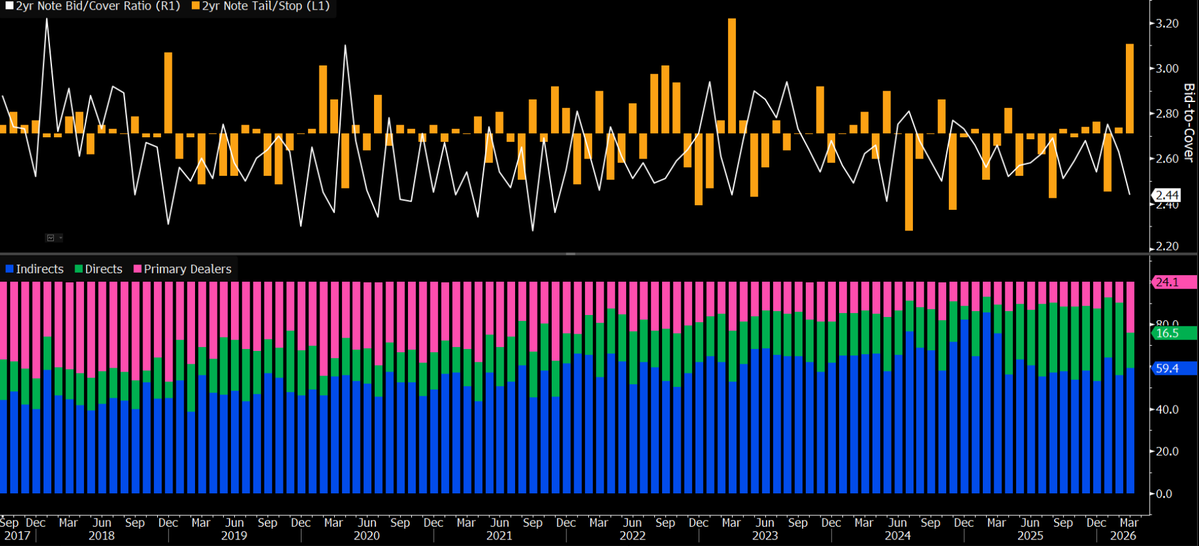

The US government continuously sells Treasuries to finance itself. Under normal circumstances, there's strong demand for them because these bonds are considered safe. But this week, the auctions went extremely poorly.

Oil-exporting countries affected by the Iran war, and investors linked to them, have played a significant role in financing the United States for years. If their revenues come under pressure due to the war, they could be forced to sell US Treasuries to raise dollars.

If large foreign buyers purchase fewer US Treasuries, this can have dangerous consequences for the financial system:

- Treasury yields rise, which pushes up other rates across the financial system.

- Borrowing becomes more expensive for the US government.

- The rest of the financial system comes under pressure from tightening financial conditions.

- The stability of the US dollar and credit markets could be at risk, with all the consequences that entails.

Wallerstein explains that we saw something similar during the COVID crisis, when the world ground to a halt and oil-exporting countries sold Treasuries to quickly raise cash.

At the time, the Fed responded with an emergency program — the so-called FIMA repo facility. This allows foreign central banks to temporarily borrow dollars from the Fed, using Treasuries as collateral.

This meant they didn't have to sell their Treasuries to raise cash, which prevented upward pressure on yields. In effect, the Fed temporarily injected extra liquidity into the system, keeping rates more stable and preventing panic.

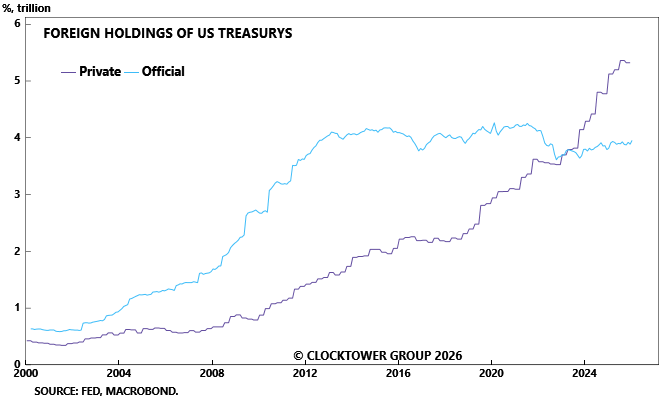

The problem is that this facility is probably insufficient for the current situation. Whereas foreign central banks used to hold the bulk of US Treasuries, an ever-larger share is now held by more private entities like sovereign wealth funds and pension funds. And those parties don't have direct access to the Fed's facility.

The solution is fairly straightforward. Give large non-US institutional investors access to this facility as well. According to Wallerstein, this could serve three goals simultaneously:

- Reduce the US government's financing costs.

- Keep financial markets more stable.

- Protect the international role of the US dollar.

In essence, Wallerstein is arguing that the Fed needs to ensure the Treasury market continues to function properly. His message is clear: intervene before higher oil prices cause more than just stress in financial markets.

5️⃣ Rates are rising — so why is the S&P 500 holding up?

Thom

Globally, the uncertainty around Iran and the Strait of Hormuz is driving yields higher. If rates keep rising at this pace, we could be heading for a 2022-style scenario, according to Jurrien Timmer of Fidelity Investments.

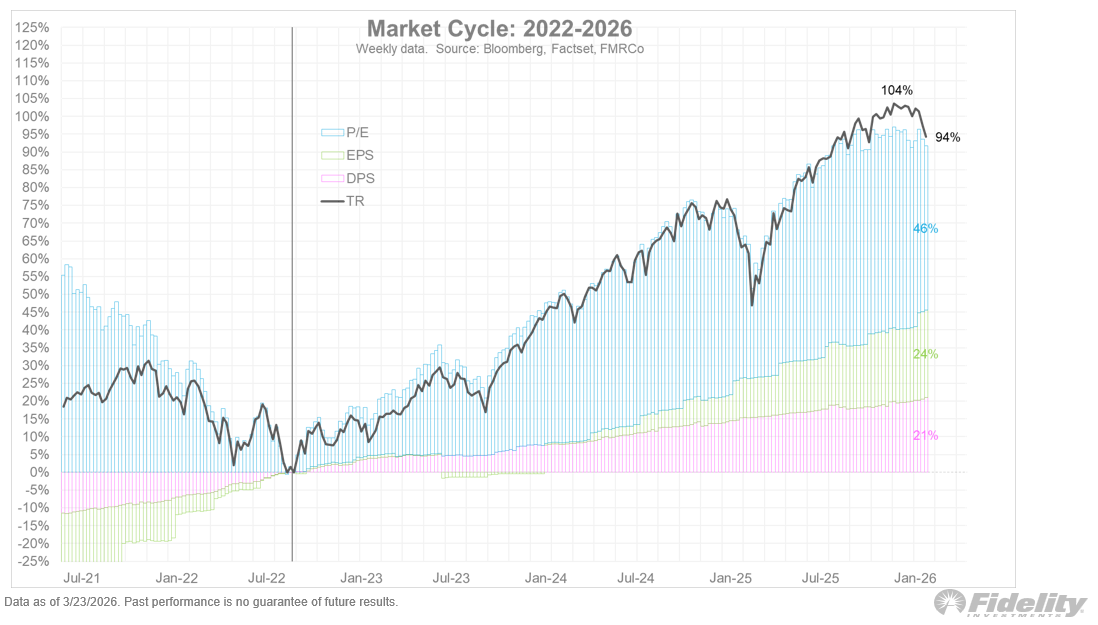

So far, the S&P 500 has dropped only about 8% from its all-time high, despite all the turmoil. How is that possible? According to Timmer, it's largely thanks to the tremendous pace at which S&P 500 earnings continue to grow.

"If corporate earnings weren't growing at double-digit rates, we'd be looking at much steeper declines right now," Timmer says.

The next chart from Timmer shows that an increasing share of returns is driven by rising earnings and dividend payments (green and pink), while speculation — expansion of the price-to-earnings ratio — plays a diminishing role.

You could say this makes the S&P 500 healthier. Speculation is fading, and stock prices are increasingly determined by hard results. Without those results, the situation would likely be far more painful right now.

For now, this seems to be keeping outright panic at bay. If the S&P 500 does decline 20% or more — officially entering bear market territory — there would likely be far more panic.

Right now there's stress, but genuine panic is still absent. To prevent that panic from materializing, a resolution to the Strait of Hormuz situation probably needs to come soon.

That matters for bitcoin too, because the momentum from the start of the war has now faded. In my view, this shows the rally happened in spite of the conflict, not because of it. To avoid losing that momentum entirely, it would be very helpful if the potential episode of full-blown panic never materializes at all.

In closing

All previous editions of Alpha Markets can be found in the archive. Questions, comments, and suggestions are always welcome in the community.

Thank you for reading!

To stay informed about the latest market developments and insights, follow our team members on X:

- Bart Mol (@Bart_Mol)

- Peter Slagter (@pesla)

- Bert Slagter (@bslagter)

- Mike Lelieveld (@mlelieveld)

We appreciate your continued support and look forward to bringing you more comprehensive analysis in our next edition.

Until then!