Geopolitical Roller Coaster

Geopolitical tensions around Iran are triggering wild swings in oil and markets, yet bitcoin remains remarkably steady. What does that say about risk appetite and investor behavior?

Peter

After forty days of war, Iran and the US reached a ceasefire last week. A two-week window to safely sit down at the negotiating table. "A great day for world peace," Trump wrote on social media. Shortly before, he had still been threatening to wipe the entire Iranian population off the map. According to Trump, virtually all points of contention had been resolved and the path was clear toward a definitive peace deal.

Financial markets responded with relief. Oil prices dropped by dozens of percentage points and green numbers appeared across many other parts of the market. The bitcoin price surged above $70,000 in no time, and the major US stock indices were once again brushing up against their record highs.

The market's reaction is very telling.

— The Kobeissi Letter (@KobeissiLetter) April 8, 2026

Amid the news of a two-week ceasefire, the S&P 500 is now nearing 6,800, trading just ~3.5% away from a new record high.

Gold prices are soaring toward $4,900/oz, Bitcoin is above $72,000, and silver is nearing $77/oz.

The reality is that… pic.twitter.com/HOknDWaTMR

It appears Trump was once again overpromising last week. The optimism that emerged is cautiously giving way to pessimism: the intended peace deal has been thrown in the bin and all American negotiators have flown home from Pakistan. No deal.

Reportedly, there were three key sticking points. Iran refuses to stop funding regional militias, such as the Houthis in Yemen, Hezbollah in Lebanon, Hamas in Gaza, and pro-Iranian militias in Iraq. Iran also refuses to open the Strait of Hormuz without conditions. And more importantly: dismantling its nuclear program is, as far as the Iranians are concerned, off the table.

The impact on financial markets was predictable: oil prices shot up, pushing the price of other assets back down.

JUST IN: Bitcoin falls under $72,000 after Vice President JD Vance says the US failed to reach a deal with Iran during negotiations in Pakistan. pic.twitter.com/RzSRDMYP59

— Watcher.Guru (@WatcherGuru) April 12, 2026

Prices haven't fallen back to pre-ceasefire levels yet. The question is what comes next. According to Washington Post columnist David Ignatius, Trump has lost his appetite for war. The new plan: apply economic pressure through a blockade of Iranian ports, then present a deal that offers economic relief.

The American blockade of the Strait of Hormuz is set to begin today at 4:00 PM. Every ship traveling to or from an Iranian port, regardless of its country of origin, will be intercepted. Is Iran likely to cave to that pressure? Based on six weeks of war, that seems unlikely. And so the conditions for further escalation are taking shape once again.

True.. pic.twitter.com/6doH3tVjDG

— Andreas Steno Larsen (@AndreasSteno) April 12, 2026

The geopolitical roller coaster is causing sharp but short-lived swings in financial markets. Despite all this, bitcoin is 'calmly' trading around $70,000, nearly 8 percent above the price at which it entered the war.

Yet that apparent calm is worth pausing over. Something doesn't quite add up.

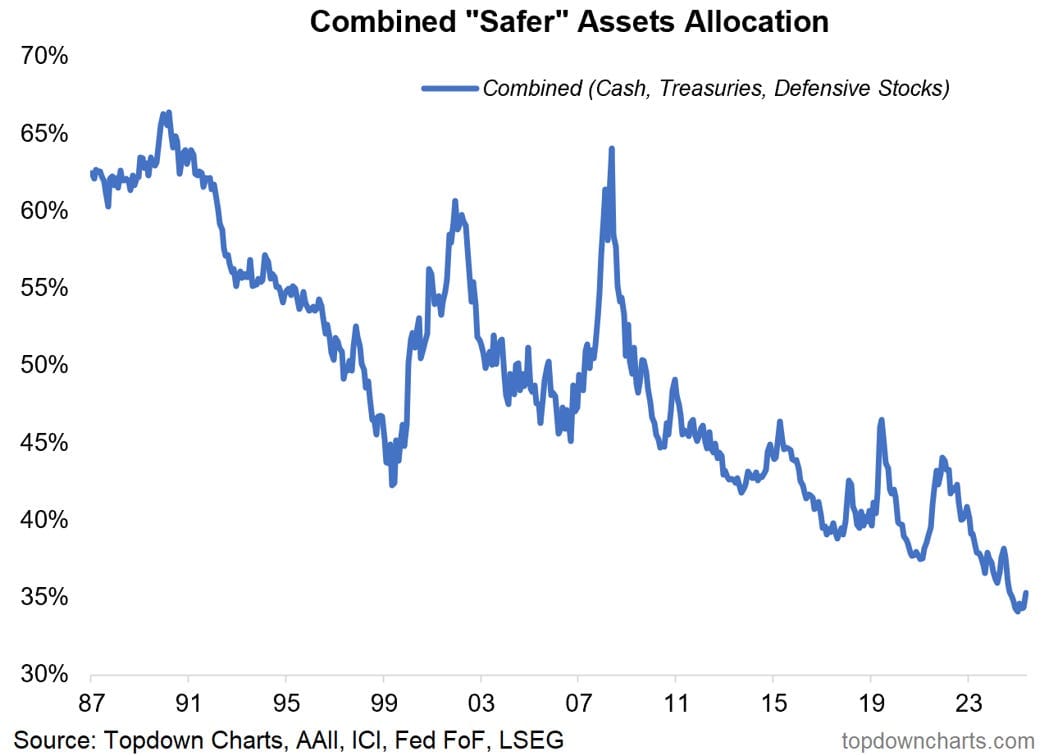

Looking at investor positioning, you see a market that's largely shrugging off geopolitical risks. Allocations to cash and bonds are at historic lows, while equities — especially tech — are in high demand. In short, investors are taking on a relatively large amount of risk.

Perhaps we're simply looking at behavior shaped by the past. For years, caution was punished and risk was rewarded. As a result, investors have grown complacent, with the accompanying feeling that hedging is unnecessary. And yet, even the most reckless gambler can't ignore the uncertainties of recent months.

An additional force may be that geopolitical stress and technological progress are balancing each other out. Behind the stream of bad news, the AI revolution is unfolding, delivering new breakthroughs month after month. Investors are trying to price that in, resulting in massive gains for specific tech companies.

This could explain why bad news barely seems to make a lasting dent in the market. As long as everyone keeps leaning the same way, the picture stays stable.

More Alpha

Are you a Plus member? Then we continue with the following topics:

- A remarkable feat of engineering: quantum-safe bitcoin transactions

- New York Times: Adam Back is Satoshi

- White House enters the stablecoin interest battle

1️⃣ A remarkable feat of engineering: quantum-safe bitcoin transactions

Erik

Imagine living in a country where the roads are controlled by armed gangs and the established authorities are powerless. If you still want to travel, you need an armored, weaponized vehicle. A new research proposal for bitcoin, published on April 9 by Avihu Levy of StarkWare, takes this approach to the looming quantum threat. He found a theoretical way to send bitcoin transactions securely, even after quantum computers become powerful enough to crack public keys.

The quantum danger for bitcoin may be approaching faster than previously thought. We wrote more about that last week.

Google recently published research showing that cracking bitcoin's cryptography would require roughly twenty times less quantum computing power than previously assumed. Google aims to have its own systems migrated to a post-quantum standard by 2029. Whether bitcoin can pull off a soft fork in that relatively short timeframe is far from certain: protocol changes have historically required a lengthy process of debate, proposals, voting, and implementation. That's a downside of a decentralized environment with many voices and opinions.

The proposal

Under the title QuantumSafe Bitcoin Transactions Without Soft Forks, the author introduces Quantum Safe Bitcoin (QSB), a series of steps that shields a bitcoin transaction from the potential power of quantum computers.

Quantum-Safe Bitcoin Transactions Without Softforkshttps://t.co/1lx5waX9VV pic.twitter.com/Ni7pA6dEsC

— Avihu Levy ✨🐺 (@avihu28) April 9, 2026

How? By shifting the security from cryptography that quantum computers are good at breaking to cryptography where they perform poorly. The digital signature — the mechanism that proves coins belong to you — currently relies on so-called elliptic curves. This type of cryptography is vulnerable to a special quantum algorithm (Shor's algorithm), which can derive private keys from public keys once computers become powerful enough.

QSB shifts the computational heavy lifting to hash functions, which even quantum computers can't reverse much better than classical computers. In QSB, the sender of a transaction does something similar to what miners already do. In mining, miners hash repeatedly until the output happens to be smaller than a certain threshold. In QSB, the sender hashes values tied to their transaction over and over until the output happens to take the form of a valid bitcoin signature.

A random hash almost never meets that criterion — the odds are roughly one in 70 trillion — so it takes significant computing power and time to find a valid output. The paper estimates the cost at around $75 to $150 in cloud computing per transaction. Not exactly for paying for a cup of coffee!

The solution found is mathematically tied to the exact contents of your transaction. If even a single byte changes, the solution no longer works and hours of computation must start over. The work you've done in advance at your leisure gives you a head start that an attacker — who can only begin once they see your transaction — can no longer overcome.

The elegant part is that the bitcoin network doesn't need to be updated for this. Nodes simply run their normal signature verification and see a valid signature. They don't know, and don't need to know, that the 'signature' is actually the output of a hash puzzle.

An emergency solution

The project is still in its infancy. So far, no QSB transaction has actually been confirmed on the bitcoin network. There's also a significant practical hurdle: QSB transactions are so large that they don't fit within the standard rules that bitcoin nodes use to relay transactions to each other. Anyone who wants to send one must deliver it directly to a miner.

And the limitations go further. QSB only works in situations where the public key doesn't become visible until the moment of sending. Millions of BTC are locked in UTXOs that more or less directly reveal the public key. In that case, an attacker can independently construct a valid transaction without having to wait for the sender.

This means QSB doesn't address the underlying problem: whoever has the private key can still spend the funds. The proposal only makes that attack more expensive and time-dependent, but not impossible.

User experience is another barrier. Creating a QSB transaction requires specialized software and substantial computing power. Instead of simply signing and broadcasting, a user must first 'find' a valid transaction. That process is so complex that it needs to be outsourced to external hardware, which further reduces accessibility.

QSB is not a structural solution, but an ingenious, temporary workaround within the existing rules. It demonstrates that quantum-safe transactions are theoretically possible without a protocol change, while simultaneously underscoring how cumbersome that is in practice. A durable solution will likely need to be found at the protocol level.

2️⃣ New York Times: Adam Back is Satoshi

Peter

The search for Satoshi Nakamoto has all the hallmarks of a modern gold rush. The identity behind this world-famous bitcoin pseudonym has taken on an almost mythical status. Every new attempt to lift the veil attracts attention. And almost always, the same pattern follows: lots of noise, little proof.

Bitcoin's founder, Satoshi Nakamoto, has remained hidden for 17 years. A trail of clues — and a year of digging by our reporter, John Carreyrou — led us to a 55-year-old computer scientist in El Salvador named Adam Back. https://t.co/s6Jy00IDdk

— The New York Times (@nytimes) April 8, 2026

Last week it was the New York Times' turn. Investigative journalist John Carreyrou, famous for his exposé of Theranos, published an in-depth piece after eighteen months of research pointing to Adam Back as the man behind Satoshi Nakamoto. A serious claim, written by a serious name. That immediately gives the article more weight than yet another blog post or documentary on the subject.

The core of his argument, however, is largely circumstantial. Back was already active in the cypherpunk movement in the 1990s, developed Hashcash — a system that closely resembles bitcoin's proof-of-work — and is moreover the only person cited by name by Satoshi in the whitepaper. Add similarities in writing style and timing, and the picture seems to fit at first glance.

But that's precisely the problem with this type of analysis: it seems to fit, until you look a little more closely.

Adam Back himself responded quickly and firmly: "I'm not Satoshi." In interviews he added that the similarities are a natural consequence of being someone who was working in the same era and environment with the same ideas. The cypherpunk movement wasn't a collection of isolated islands, but a network where ideas, code, and language were constantly shared and reused. Anyone searching for unique characteristics within that space will quickly find patterns that aren't really there.

i'm not satoshi, but I was early in laser focus on the positive societal implications of cryptography, online privacy and electronic cash, hence my ~1992 onwards active interest in applied research on ecash, privacy tech on cypherpunks list which led to hashcash and other ideas.

— Adam Back (@adam3us) April 8, 2026

Similar criticism is echoing within the bitcoin community. Not so much out of loyalty to Back, but from experience. After all, this isn't the first time someone has been put forward with conviction. Dorian Nakamoto, Craig Wright, Peter Todd — every time the same cycle follows: accusation, denial, and debunking. Wright is the most extreme example: years of claims, lawsuits, and ultimately a judge ruling that he had simply lied.

What stands out is that the evidence rarely goes beyond circumstantial clues. Stylometry, timelines, technical influences. Interesting, but not conclusive. Certainly not in a world where anonymity was a deliberate choice from day one.

There are also substantive counterarguments. Programmers point out that Adam Back's code differs fundamentally from Satoshi's. Others note that Back only became active on bitcoin forums after Satoshi had already disappeared. These aren't definitive proofs, but they do underscore how fragile the puzzle is.

And that may be a good thing. Satoshi's anonymity has shaped bitcoin into what it is: a system without a face, without a leader, and without a central authority. Everyone can assign their own meaning to it. The project is not tied to a person, and therefore not vulnerable to their mistakes, beliefs, or self-interest.

Every new 'unmasking' is therefore unsatisfying by definition. If the evidence is paper-thin, the analysis lands on the pile of previous attempts. And if someone actually succeeds in identifying Satoshi? Then bitcoin loses one of the most beautiful aspects of its origin story.

But you can bet on it: this won't be the last attempt. On April 22, the documentary Finding Satoshi drops. Will it deliver the definitive verdict?

3️⃣ White House enters the stablecoin interest battle

Peter

On April 8, the White House published a striking report on a seemingly technical question: should stablecoin issuers be allowed to pass interest through to their users? Behind that question lies a battle that now occupies the very heart of American financial policy.

The report, prepared by the Council of Economic Advisers (CEA), attempts to shift the debate with hard numbers. The conclusion is sharp: a ban on interest payments barely benefits banks, but it does cost consumers money. According to the model, bank lending in this scenario would increase by just $2.1 billion — a negligible 0.02 percent of the total. Against that stands a loss of roughly $800 million per year for stablecoin users who miss out on interest.

Stablecoins like USDC and USDT are backed by reserves, often in short-term US Treasuries. Those earn interest. The question is: does that interest stay with the issuer, or does it (partially) flow back to the user? Coinbase, for example, offers 3.5 percent interest on USDC. For banks, that's a direct threat. Savers could move their money, and with it disappears a cheap source of funding.

The White House largely dismisses those concerns. Banks can adapt, the economists argue — for example, by offering higher rates or attracting alternative funding. Moreover, the money continues to circulate in the economy, they say, because stablecoin reserves are invested in Treasuries.

But that's precisely where the tension lies. Banks don't primarily look at credit volumes, but at their balance sheets. Deposits are their foundation. If those shift to stablecoins, their business model changes, even if total lending barely moves. The banking lobby also points to tail risks: in a stress scenario, a rapid outflow of deposits could put smaller banks under pressure.

The report acknowledges that dynamic only in passing, and that's no coincidence. The CEA advises the president, and the current administration is clearly taking sides in favor of the crypto sector. The timing underscores that. The Senate is currently negotiating the Clarity Act, in which the question of stablecoin interest is a key sticking point.

What remains is a shift in the playing field. Banks long dominated the debate with warnings about financial stability. Now the White House is emphasizing consumer welfare. That flips the burden of proof. It's no longer the crypto sector, but the banks that must demonstrate their risks outweigh the foregone returns for millions of users.

🍟 Snacks

To wrap things up, some quick bites:

- Morgan Stanley's bitcoin ETF is live and immediately attracted tens of millions. The fund ($MSBT) pulled in over $30 million on day one and, with low fees, has launched an assault on existing ETFs. Coinbase serves as custodian and is benefiting from the inflows. The message: institutional inflows keep coming, regardless of short-term price action.

- Iran wants ships in Hormuz to pay tolls in bitcoin. According to an Iranian regime spokesperson, a fee of $1 per barrel must be paid. Although the statement specifically mentions bitcoin, analysts expect Iran will ultimately prefer to use stablecoins. For Iran it's a logical move: the country wants to circumvent sanctions and secure revenue. If bitcoin is actually used, it would suddenly take on a geopolitically highly sensitive role.

- Hacker creates 1 billion DOT out of thin air and dumps it immediately. Through a vulnerability in a bridge contract, the attacker was able to mint Polkadot tokens on Ethereum and sell them, netting approximately $237,000 in profit. The damage was limited due to low liquidity. On the Korean exchanges Upbit and Bithumb, DOT trading was temporarily halted. Polkadot itself was unaffected; the project points to shortcomings in the Hyperbridge interoperability protocol that was used.

- Stablecoins could grow into dominant payment infrastructure. Chainalysis estimates that stablecoin economic transaction volume could reach $719 trillion by 2035. The analytics firm cites two underlying trends. First, the transfer of roughly $100 trillion in wealth to younger generations who use crypto more frequently. Second, the integration of stablecoins into payment flows, making transactions faster and cheaper. If this trend continues, traditional payment networks could come under pressure.

- Pepe ETF filed, but Wall Street stays away from memecoins. The market barely reacted to the application filed by asset manager Canary. That fits a broader pattern. Existing Dogecoin ETFs are barely attracting capital: just $13 million in inflows this year. Beyond bitcoin, ether, solana, and XRP, interest is thin. Institutional investors still struggle to build a serious investment case around memecoins.

Thank you for reading!

To stay informed about the latest market developments and insights, follow our team members on X:

- Bart Mol (@Bart_Mol)

- Peter Slagter (@pesla)

- Bert Slagter (@bslagter)

- Mike Lelieveld (@mlelieveld)

We appreciate your continued support and look forward to bringing you more comprehensive analysis in our next edition.

Until then!