From Vienna to Bitcoin

From Hayek's break with socialism to the rise of bitcoin: how ideas about knowledge, prices, and decentralization culminated in a monetary system without central authority.

Peter

In the early 1920s, the young Friedrich Hayek was, by his own account, a "mild Fabian socialist." He lived in difficult times. The Habsburg Empire had collapsed, the economy was in ruins, and sky-high inflation had turned money into a melting phenomenon. Hayek and his fellow students were convinced that capitalism bred inequality and had enabled the war that ended so catastrophically just a few years earlier.

Because the existing order had so clearly failed, the desire to radically reorganize the economy was only natural. Like an engineer running a factory, for instance. Let a central government decide what gets produced and how the costs and benefits are distributed.

Hayek on what cured him of socialism:

— F. A. Hayek Quotes (@FAHayekSays) March 29, 2026

"I turned to economics because I was half a socialist. I was crying for social justice. But it didn't long survive my study of economics."

"In 1922, when I was 23, Mises's book on socialism came out—and that cured me forever." pic.twitter.com/PbOmYHBWJF

But this appealing idea has a fundamental problem. Ludwig von Mises exposed it in a 1920 article that two years later grew into the book Die Gemeinwirtschaft.

When the state produces everything, the required raw materials are no longer traded. A state-owned factory doesn't buy steel from a state-owned mine — it simply gets allocated. With that, prices disappear too, and prices are the only yardstick an economy has for comparing choices. Is steel better used here than wood over there? Is a bridge more valuable than a railway? The central planner can make decisions, but cannot test them against economic reality. In short, the system has no compass.

For Hayek, this was the turning point. The question was no longer whether the goal was noble, but whether the system could work. Over time, he formulated what became known as the knowledge problem. The knowledge needed to coordinate an economy, he argued in 1945, doesn't reside in one place. It is dispersed across millions of people, embedded in local circumstances, and subject to changing preferences. No single entity can fully collect that knowledge, let alone process it.

Prices, in this reading, are not a byproduct of markets but their nervous system. When the price of a commodity rises, producers and consumers adjust their behavior without needing to know the cause. For Hayek, the question therefore became a different one: not who has enough oversight to steer everything, but which system makes use of the knowledge that already exists. His answer was the least bad information system he knew of: the free market.

The underlying idea — that concentrating decision-making undermines its quality — surfaces in a variety of places. Alexis de Tocqueville observed in the 1830s how Americans organized locally, in associations and ad-hoc gatherings. The strength of their democracy, he noted, lay in the habit of solving problems themselves. If that habit disappears and everything shifts to the center, citizens become spectators.

Among Catholics, this principle got a name. In a weighty letter, the Pope wrote in 1931 about subsidiarity. What can be handled locally should stay local. But when a municipality or community truly cannot manage something, the authority above should step in — not to take over, but to assist.

Later thinkers gave this an empirical foundation. Elinor Ostrom demonstrated that local communities can manage complex systems without central control, as long as they have clear rules and feedback mechanisms. She won the Nobel Prize for it in 2009. Nassim Taleb pointed to the risks of scale. Small systems fail locally and recoverably; large systems fail all at once, with far less graceful consequences.

Well into the twentieth century, this remained an intellectual debate. How much centralization is desirable? Where is the line? How much influence should a citizen have? Which decisions should they be allowed to make themselves?

Until then, the answer had always been institutional. Better rules, for instance, or a better distribution of powers. But rules need enforcement, and enforcement requires trust in the enforcer.

In the 1990s, a movement emerged that saw that trust itself as the weak link. The cypherpunks, a loose group of programmers and cryptographers, shared the skepticism toward central power but chose a radically different solution. Instead of designing better institutions, they built systems where trust is less necessary.

Bitcoin is a child of this movement. On October 31, 2008, Satoshi Nakamoto described an electronic cash system without a central issuer. Through a technical design, he translates the older insights into new infrastructure. Bitcoin allows prices and transactions to emerge again without a central authority. Subsidiarity advocates for decision-making at the lowest possible level; bitcoin eliminates the higher level for one specific function entirely.

The line from Vienna to bitcoin is, of course, less straightforward than it appears. Yet a recognizable thread runs through it. An initially ideological project — the improvement of society — runs into the limits of knowledge and coordination. That leads to a reappreciation of spontaneous order and small-scale organization. And eventually, the question shifts from who governs to how you build systems that work without a governor.

Hayek started as someone who wanted to make the world more just. That ambition didn't disappear, but it took on a different character. The question became which system is least dependent on trustworthy decision-makers making perfect decisions. In a century where states and networks are gaining in scale, that distinction is — to put it mildly — relevant once again.

More Alpha

Are you a Plus member? Then we continue with the following topics:

- Fidelity: 10% BTC in a portfolio is defensible

- Clarity Act negotiations stall again

- Tether finally gets a serious audit

1️⃣ Fidelity: 10% BTC in a portfolio is defensible

Erik

Last week, American asset manager Fidelity published a report (Getting Off Zero: Bitcoin in 2026). The central question it aims to answer: what is a reasonable percentage of BTC in your portfolio? A few conclusions: having zero BTC in your portfolio is hard to justify. And: a 10 percent allocation is well defensible.

Fidelity, the provider of the second-largest bitcoin ETF, has been researching the digital assets space for years. The fact that the title of this well-written report contains Getting Off Zero is a nod to the bitcoin community, which has used this slogan for years to give existing and new investors a framework for thinking about bitcoin.

Namely: it's a risk to have no BTC in your portfolio at all. You're then not exposed to the price of an asset that could still fail, but has an asymmetrically high upside. Prominent American investor and media figure Anthony Pompliano was one of the first to promote Get Off Zero in 2018 on Twitter and in television interviews.

Here is an example of how we meme'd bitcoin onto Wall Street.

— Anthony Pompliano 🌪 (@APompliano) March 26, 2026

Back in 2018, a friend told me about an old marketing campaign that suggested investors "get off zero" in terms of their allocation away from cash, bonds, and real estate.

I borrowed the idea and applied it to… pic.twitter.com/7YDLAmyBMI

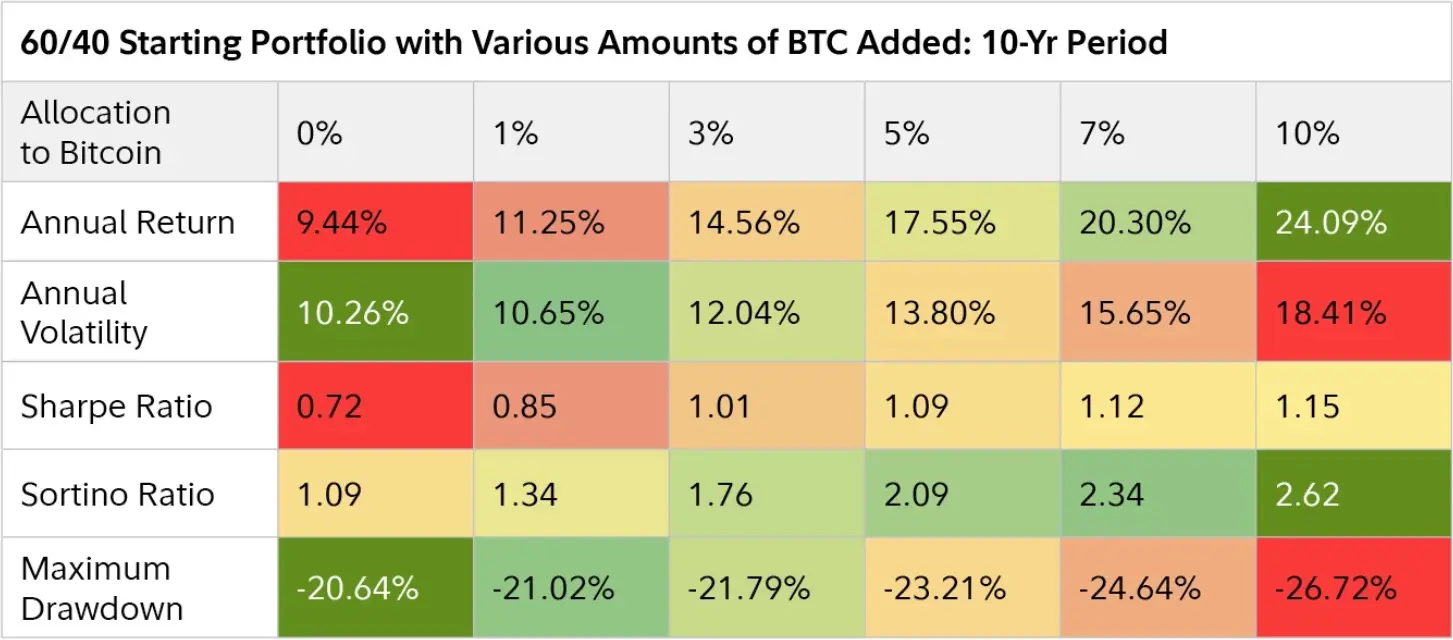

In the report, Fidelity quickly concludes that BTC is well defensible in portfolios. Measured over ten years, bitcoin's risk-adjusted return is better than stocks or bonds. Additionally, the correlation with traditional assets is low. That latter point is also important for portfolio managers.

What percentage of BTC in a portfolio?

Fidelity doesn't rule out that a zero allocation might still be a defensible option for some asset managers. But that's now a minority view. The question that follows is:

"The central question is no longer whether bitcoin deserves consideration in a portfolio, but rather: What is your current bitcoin allocation, and why?"

To answer this, Fidelity looks at returns, volatility, and the resulting risk over ten-year and five-year periods in the past. The difference between those periods is substantial: over the past five years, BTC hasn't performed exceptionally well; so it's fair that Fidelity includes that period too.

Fidelity calculates that bitcoin achieves a better Sharpe ratio — return versus risk — than stocks, bonds, and gold. A Sharpe ratio below 1 is inadequate; bitcoin sits well above that, at least when viewed over the ten-year period.

The Sortino ratio, which only weighs downside volatility, is even more favorable: bitcoin has historically exhibited more "good volatility" in the form of sharp rallies than bad. Even over the past five years, a period in which BTC performed less exceptionally, the pattern holds.

An interesting finding from the simulation: both the Sharpe and Sortino ratios rise as the BTC percentage grows from 0 to 10 percent. A 10 percent allocation is therefore better by key metrics than 1 percent. Not only is the return higher, the risk-adjusted return is also more favorable.

Where does the BTC allocation come from?

Fund managers used to view bitcoin as an alternative to equities. Lately, that's been shifting. Due to the disappointing performance of bonds, the allocation increasingly comes from the bond bucket. Fidelity concludes, however, that the choice hardly matters:

"The biggest difference in results came from the decision to get off zero — the choice of which bucket to fund the allocation from resulted in very marginal differences."

Kelly Criterion as the foundation

A remarkable finding in the report is the quantitative foundation behind Get Off Zero. How large should your BTC allocation be? They use the Kelly Criterion for this. It's a formula applied to gambling and investment strategies. It weighs four things against each other: how often you win, how often you lose, how large the average win is, and how large the average loss is. The greater the asymmetry between wins and losses — meaning the more you win on average relative to what you lose — the higher the optimal bet turns out.

Using bitcoin's historical numbers as input, the formula calculates an optimal BTC allocation in a portfolio of 65 percent! While the report's author admits that institutional investors would never be allowed to choose such a high allocation, the insight the Kelly Criterion provides remains:

When an investment opportunity exhibits a positive expected return and a highly asymmetric payoff—meaning the potential upside significantly outweighs the potential downside—the most "efficient" position size may be larger than what investors intuitively think.

Perhaps the new slogan should be: Get Off 5%. Because even with the conservative inputs in the model of 25 percent returns in good years and a maximum drawdown of 50 percent in bear market years, the Kelly Criterion still arrives at a 10 percent BTC allocation in a portfolio.

2️⃣ Clarity Act negotiations stall again

Peter

Negotiations over the American Clarity Act are in their decisive phase. The law, which you could think of as the U.S. counterpart to MiCA, is meant to clarify how crypto fits into the financial system. Market participants broadly agree on the big picture, but the devil is... once again in the details.

The major sticking point remains stablecoin yield. In the most recent draft, interest on "passively" held stablecoins is effectively banned. Only incidental rewards tied to usage would still be permitted. Banks, eager to preserve their monopoly on offering interest on dollars, are once again coming out on top. They want to prevent capital flight from the traditional system — a card that apparently plays well at the negotiating table.

But for the crypto sector, offering yield is part of the business model. Coinbase uses it to attract new users, for instance, and companies like Circle owe much of their growth to it indirectly. It's no surprise that Circle's stock dropped 20 percent after the new text leaked — its worst day on the market ever.

Because the negotiations keep producing the same outcome, some parties within the industry are cutting their losses. For them, an imperfect law is better than no law, because it finally provides institutional clarity.

But heavyweight Coinbase isn't ready to concede. The company is walking the line between influence and opposition. Publicly, Coinbase voices strong criticism of the proposal, while behind the scenes it's working on a counterproposal. According to Coinbase analyst David Duong, a solution for the outstanding issues needs to be on the table within three weeks. If Congress then prioritizes the bill, a final decision could come in May.

CLARITY Act -- issues and timeline. On the crypto policy front, the CLARITY Act moved back into focus this week as stablecoin rewards once again emerged as a key sticking point. Recall that there was an announcement from Senators Thom Tillis (R-NC) and Angela Alsobrooks (D-MD)…

— David Duong🛡️ (@DavidDuong) March 27, 2026

That timeline seems somewhat optimistic. The next two weeks will offer little clarity, as the U.S. Congress is on Easter recess. After that, formal talks will resume, but most policy watchers don't expect the bill to change significantly. From the outside, they appear to be right!

3️⃣ Tether finally gets a serious audit

Peter

Tether, the issuer of the world's largest stablecoin USDT, is getting a thorough examination through a full audit by a Big Four firm. KPMG will audit the books, and PwC will prepare the internal organization to pass that test. Tether is finally getting what the market has been waiting years for: a real financial audit.

Tether hires KPMG as auditor ahead of US expansion https://t.co/xE2uB42DLU

— Financial Times (@FT) March 26, 2026

Until now, monthly reports from BDO Italia provided a snapshot of the reserves. Useful, certainly, but also limited. An audit goes much deeper. You're not just looking at what's there, but how it got there. Processes, internal controls, documentation, governance — nearly everything is scrutinized. When it comes to assurances, that's a world of difference.

Not long ago, Tether received a multimillion-dollar fine from regulator CFTC over misleading communication about USDT's backing. Earlier attempts to complete an audit fell through prematurely. The promise was always there, but the follow-through never came.

That such an audit is now possible also has to do with the changing times. Stablecoins as a phenomenon have become more mainstream, making auditors willing to even consider their involvement. After the signing of the Genius Act, the American stablecoin law, there's also a legal basis for it. At the same time, Tether is actively seeking to connect with institutional investors and the U.S. market. An audit is then not an optional luxury, but a requirement. Without credible numbers, the door stays shut.

Tether now manages roughly $185 billion in reserves, mostly in U.S. government debt. This makes the company not only a critical link between the crypto world and the traditional financial system, but also a top-20 player in the government bond market.

Anyone who thinks this audit will answer all questions is primarily looking at the accounting — not at the role Tether now plays in the system. Still, after this, a significant chunk of the persistent Tether FUD can finally be crossed off the list!

Tether will never produce an audit.

— Parrot Capital 🦜 (@ParrotCapital) March 24, 2026

You can't audit a money laundering fraud.

It will never reconcile. https://t.co/2zA98UTfH1

🍟 Snacks

To wrap up, a few quick bites:

- Morgan Stanley aims to crack open the bitcoin fund market with low fees. The bank plans to offer its new bitcoin fund at a management fee of 0.14%. That undercuts existing products, including those of rival BlackRock. The pricing strategy could help capture market share quickly. The bank's extensive network of wealth advisors is a second key weapon. ETF watchers expect the fund to open its doors within two weeks.

- UK wants to ban crypto donations to political parties. The Starmer government is stepping in amid concerns over foreign influence through hard-to-trace money flows. Crypto is seen as a potential backdoor. The proposal follows an independent review and still needs parliamentary approval. Donations in traditional currency remain permitted, even for parties with ties to the crypto sector. In Canada, the government is on a similar track.

- JPMorgan: bitcoin is increasingly behaving like a safe haven. During the Iran crisis, capital flowed into bitcoin while investors were exiting gold and silver. According to the bank, this points to a shift in how investors handle geopolitical uncertainty. In countries like Iran, crypto usage also increased as citizens tried to protect their wealth from economic instability and capital restrictions.

- Strategy expands capital capacity for bitcoin purchases. Michael Saylor's company aims to raise up to $42 billion in new capital. This involves a combination of equity offerings and preferred financing, spread across multiple programs. Data from CryptoQuant shows that Strategy is now responsible for more than 75 percent of bitcoin demand among publicly traded companies. It underscores Strategy's dominance, but also the one-sidedness of this segment of the market.

- Americans can use crypto as collateral for a home down payment. Better Home & Finance introduces the new lending option in partnership with Coinbase. Customers can put up bitcoin or USDC to free up dollar liquidity. This structure makes it possible to maintain bitcoin exposure while deferring tax payments. The loan doesn't replace a mortgage — it's on top of one.

- DeFi is less decentralized than often thought. That's the finding of the ECB in a recently published paper, which applies supervisory questions to this emerging market. In major protocols like Aave and Uniswap, a large share of governance tokens turns out to be held by a small group, often linked to the protocol itself or to exchanges. Decision-making is also heavily concentrated. Votes are mostly delegated to a small number of parties, whose identities are often unknown.

Thank you for reading!

To stay informed about the latest market developments and insights, follow our team members on X:

- Bart Mol (@Bart_Mol)

- Peter Slagter (@pesla)

- Bert Slagter (@bslagter)

- Mike Lelieveld (@mlelieveld)

We appreciate your continued support and look forward to bringing you more comprehensive analysis in our next edition.

Until then!